Aggregator Impact on Brands

How Platforms Intercepted the Moment That Loyalty Used to Own

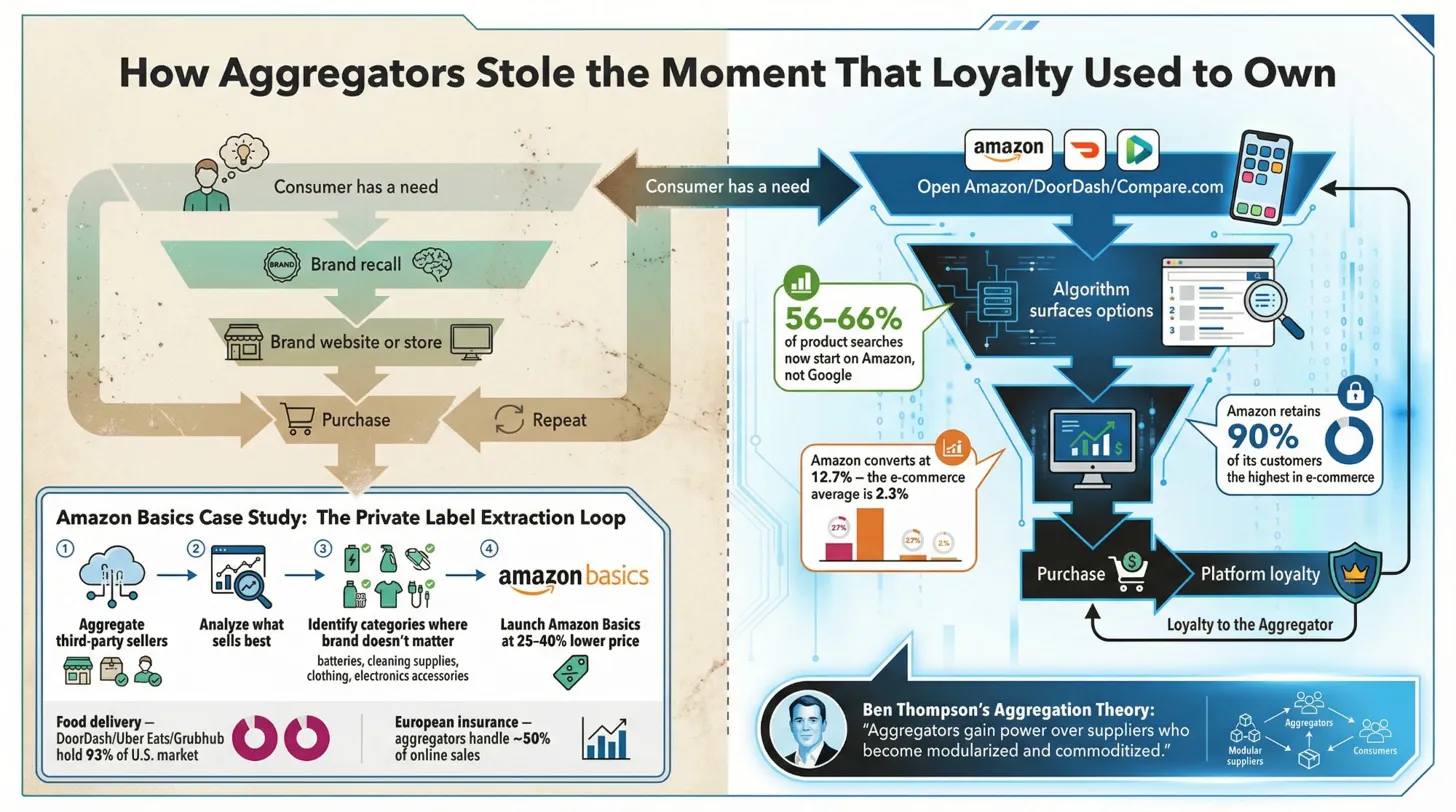

The aggregator funnel, in one image.

The old brand-owned loop ran from need to brand recall to direct channel to purchase. The aggregator loop intercepts at step one — and owns every step that follows.

“Aggregators gain power over suppliers who become modularized and commoditized. The consumer relationship migrates to the platform. The brand becomes a row in a search result.”

How the loyalty moment was stolen.

The old purchasing loop was brand-controlled. A consumer had a need, recalled a brand, visited the brand's channel, purchased, and repeated. The aggregator loop intercepts at step one — before brand recall ever fires.

The Consumer Came to You

Need fires

Hunger, a broken appliance, a new outfit.

Brand recall fires

Memory of a positive experience surfaces the brand unprompted.

Brand channel visit

Consumer navigates directly to the website, store, or app.

Purchase completes

The brand owns the transaction and the data.

Loop deepens

The relationship tightens with each cycle, building generational equity.

The Consumer Goes to the Platform

Need fires

The same trigger as before.

Open Amazon / DoorDash / compare app

The platform intercepts before brand recall fires. The habit has been trained.

Algorithm surfaces options

Your brand competes on price, rating, and sponsored placement. Brand equity is largely irrelevant.

Purchase completes

The platform owns the transaction, the data, and the relationship.

Loyalty migrates to the aggregator

The loop tightens around the platform. Your brand is interchangeable supply.

The Amazon Basics extraction loop.

Amazon's private-label strategy is the most clinical demonstration of what platform power over suppliers looks like in practice. It is not accidental. It is a four-step extraction architecture.

Aggregate sellers

Third-party brands list on the platform to access Amazon's 300M+ active customers. They pay fees, accept terms, and surrender transaction data.

Analyze what sells

Amazon has complete visibility into which products move, at what price, with what return rates. No third-party brand has equivalent data on its own category.

Identify commodity gaps

Categories where brand differentiation is weak — batteries, cleaning supplies, basics, accessories — become targets for displacement.

Launch at 25–40% lower

Amazon Basics enters with structural cost advantages — no marketing spend, preferential placement, built-in Prime loyalty. The original brand cannot compete on its own platform.

The deeper lesson: Amazon Basics does not win because it is a better product. It wins because the platform has eliminated the conditions under which brand equity could have protected the original brand. The extraction loop only works on brands that were already commodities in disguise. Price and placement beat story and relationship — when the platform controls price and placement.

Where aggregator control is already total.

Food Delivery — Restaurants Lost the Relationship

DoorDash, Uber Eats, and Grubhub collectively control 93% of U.S. food delivery. The restaurant's logo appears on the app — but the platform owns the consumer relationship, the data, the reorder habit, and the loyalty program. The restaurant is a kitchen with a logo.

Product Discovery — Search Gravity Has Migrated

More than half of all product searches now begin on Amazon — not Google, not brand websites. Brand awareness that does not convert to platform presence is increasingly unreachable equity: built but inaccessible at the moment of purchase.

European Insurance — The Trust Moment Was Captured

Aggregator comparison sites handle roughly half of online insurance sales in Europe. The insurer's brand — historically built on trust and relationship — is reduced to a price column in a comparison table. The trust moment now belongs to the aggregator.

Grocery & CPG — Private Label Eats the Middle

Retailer private-label brands grew 3× faster than national brands in 2024–25. The aggregator-as-grocer (Amazon, Walmart, Costco, Aldi) controls shelf placement, pricing, and consumer data — and uses all three to launch competing house brands at structurally lower cost.

“Amazon's 12.7% conversion rate is nearly 6× the e-commerce average. That gap is not closeable through better UX or more ad spend. The platform eliminated payment friction, solved the trust problem, and trained habitual behavior over two decades — and a 90% retention rate means that once a consumer adopts the platform as their default, the brand has less than a one-in-ten chance of recapturing direct engagement in any given renewal cycle.”

What brands lose — and how some are fighting back.

The aggregator threat is not merely competitive. It is structural — a rewiring of who owns the consumer relationship. Understanding what is actually at risk clarifies what is worth defending.

The consumer relationship migrates to the platform.

Every purchase completed through an aggregator is a data point that belongs to the platform. The brand learns nothing — no purchase frequency, no co-purchase patterns, no lapse signals. Relationship intelligence accumulates at the platform and erodes at the brand.

Brand salience becomes unreachable.

When 56–66% of product searches begin on Amazon, awareness built through advertising may not convert to consideration — the consumer never reaches a channel where that awareness matters. Marketing spend can generate equity that has no purchase path.

Generational equity decays without direct contact.

Brand equity with younger generations requires direct engagement to form. If a Gen Z consumer's first and primary interaction with a brand is through an aggregator's interface, the generational equity relationship never starts.

Build direct relationship infrastructure first.

Brands that are winning invest in owned channels before they need them — email lists, loyalty programs, community platforms, subscription models. The goal is not to avoid aggregators but to ensure the direct relationship is deep enough to survive aggregator dependence.

Build salience that survives platform intermediation.

Brands that retain salience through aggregator layers have strong identity signals — distinctive visual language, cultural resonance, community, craft signals that consumers actively seek rather than passively accept.

Treat the direct channel as generational-equity infrastructure.

The direct channel is the only place where the brand can speak, demonstrate craft, accumulate trust, and build a generational relationship. For younger cohorts especially, that contact needs to feel like a genuine exchange — not a transaction dressed up as a relationship.

Each cohort experiences aggregator power differently.

The aggregator's grip is not uniform across generations. Platform habituation depth, the strength of pre-existing brand relationships, and accumulated generational equity all shape how each cohort navigates — or surrenders to — platform intermediation.

Platform-native, brand-agnostic by default.

Gen Z formed consumer habits inside aggregator environments. TikTok Shop, Amazon, and comparison apps are not alternatives to brand channels — they are the default first step. Brand recall barely registers before platform search fires. For brands, this cohort represents a generational-equity cold-start problem: the relationship has to be built from zero inside an environment controlled by the platform.

Converted to aggregators during peak relationship-building years.

Millennials experienced the migration in real time — early brand relationships, then Amazon Prime and app-based platforms gradually capturing purchase defaults during their twenties and thirties. Many maintain residual direct relationships with specific brands they trust deeply, but their default behavior is platform-first.

The most recoverable cohort for direct relationships.

Gen X formed its deepest brand relationships before aggregator dominance. Those relationships carry real generational-equity weight — and many Gen Xers actively seek direct brand engagement when the experience justifies it. They are the most likely cohort to choose a brand's direct channel over an aggregator if the brand makes a compelling case.

Highest equity, most underserved by platform design.

Boomers carry the deepest pre-aggregator brand relationships of any living cohort. Many still prefer direct channels — and are frequently frustrated by aggregator interfaces designed without them in mind. They represent a significant direct-channel opportunity that brands systematically underinvest in.

Strategic imperatives in the aggregator age.

Platform presence is not optional. But platform dependence is a strategic vulnerability. The brands that survive the aggregator era will use platforms without being owned by them.

Use platforms. Do not be defined by them.

Platform presence is table stakes for discovery. But a brand whose entire consumer relationship exists inside a platform has no brand equity — it has a listing. The direct channel must be built, tended, and treated as the primary equity-building environment.

Measure equity you can actually spend.

Brand awareness and preference scores disconnected from direct-channel behavior are theoretical assets. The relevant question is: does our equity actually pull consumers out of the aggregator loop and into a direct relationship?

The commodity test is the aggregator test.

If your product can be replicated by Amazon Basics at 30% lower with no meaningful consumer resistance, you were always a commodity. The aggregator revealed the vulnerability — it did not create it.

Generational equity cannot be built on a competitor's platform.

Trust, identity, and relationship — the components of generational equity — require direct contact over time. A brand that only exists for younger cohorts inside an aggregator's interface cannot build equity that survives a platform change.

AI agents are the next aggregator frontier.

As AI shopping agents become the default purchase interface — surfacing options, comparing prices, completing transactions — aggregator intermediation intensifies. A brand that cannot be retrieved by an AI agent without a human in the loop has a platform problem about to get worse.

The brands that survive will own a community, not just a customer list.

Aggregators cannot intermediate a genuine community. Brands that invest in real relationships — forums, loyalty ecosystems, craft communities, shared purpose — create a structural moat that platform economics cannot easily replicate.

Share Your Voice

Join the conversation to share your thoughts and help others understand this topic better.

Join the ConversationCommunity Feedback

No comments yet. Be the first to share your thoughts!