The Barbell Brand Experience

Two Poles, One Bar, and a Middle That Will Not Recover

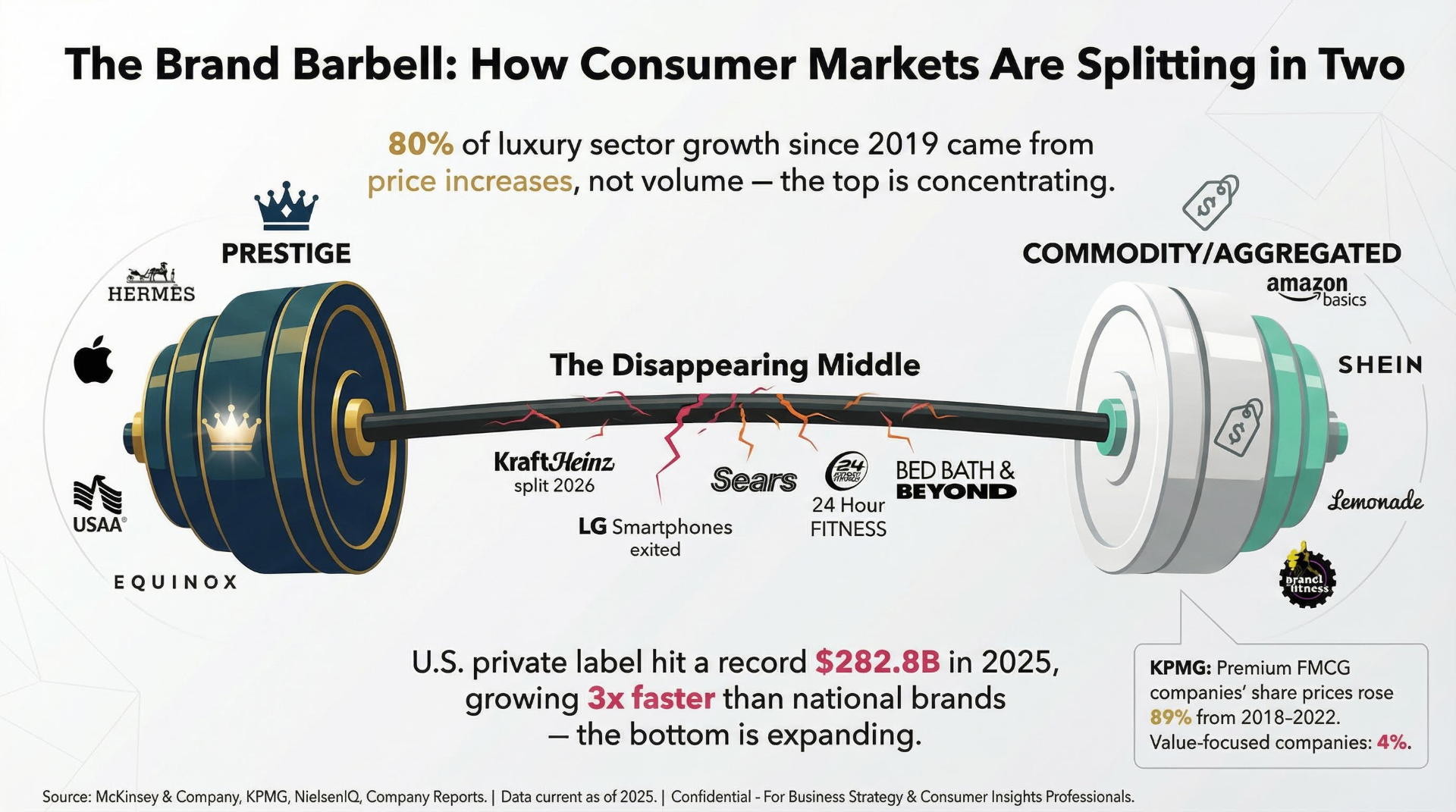

The brand barbell, in one image.

The shape of the modern consumer market is no longer a bell curve. It is a barbell: weight concentrated at the prestige pole on one end and the commodity pole on the other, with a thinning bar of mid-market brands stretched dangerously between them.

“The middle was never just a price point. It was a promise — that consistent, reliable, reasonably priced brands could earn enduring loyalty. That promise has been broken simultaneously by aggregator platforms, generational trust deficits, and an AI-accelerated race to the bottom on undifferentiated output.”

Five forces pulling the bar apart.

The Prestige Pole is Concentrating

Luxury, premium-with-meaning, and identity-affirming brands are capturing a rising share of consumer profit pools — but only those backed by genuine craft and accumulated generational equity. Legacy IP without a living creative spark eventually loses gravitational pull.

The Commodity Pole is Expanding

Private label, ultra-low-cost platforms, and aggregator-mediated transactions are redefining baseline expectations. Survival here demands logistics mastery, ruthless margin discipline, and the courage to never pretend to be more than what you are.

Mid-Market Brands Are Disappearing

Sears, Bed Bath & Beyond, mid-tier department stores, regional chains, and 'reliable national brand' SKUs across grocery and hardlines are losing share every year. The middle is not a stable position — it is a no-man's-land.

Aggregators Tax Every Transaction

Amazon, TikTok Shop, Instacart, DoorDash, and emerging AI shopping agents serve the transaction, not the brand. Every brand that builds primary discovery on a platform pays an equity toll on every sale and rents access to its own customers.

Craft Is the Surviving Signal

When AI floods the middle with competent-but-undifferentiated output, the only signal that survives is genuine craft — real formation, real standards, real human judgment applied over time. Craft is the new defensible moat.

The brands that didn't choose.

The middle is not a stable position. It is a no-man's-land — too expensive to win on price, insufficiently differentiated to command loyalty. These brands did not fail because markets changed. They failed because they believed familiarity was enough.

“We did not just lose middle-tier brands. We lost the mechanism that rewarded building something genuinely good over a sustained period of time. The market no longer has patience for the journeyman. It wants the master immediately — or the disposable cheaply.”

Each generation reads the barbell differently.

Generational equity — the accumulated trust or distrust each cohort carries toward institutions and brands — shapes which pole feels accessible, authentic, or worth pursuing at all.

Radical value, or identity-affirming premium.

Entering adulthood with negative generational equity toward institutions, Gen Z does not assume brands deserve loyalty. Under affordability pressure, they default to platform-aggregated commodities — but when they do invest, it is in brands that signal authentic identity with near-religious intensity. The middle reads as dishonest to them.

The generation that watched the promise break.

Millennials were the last cohort sold the middle-class brand promise and the first to see it voided. Student debt, the 2008 collapse, and gig work compressed their generational equity with traditional institutions to near zero. They invented premium-with-meaning — then got priced out of it by inflation.

The hinge generation — craft memory intact.

Gen X apprenticed in the old model and survived into the new one. They remember when brand loyalty was a reasonable bet. Now in peak earning years, they can access the prestige pole — but carry healthy skepticism that premium branding is often legacy IP running on fumes. They reward craft they can verify.

Renegotiating decades of brand relationships.

Boomers built their brand relationships before the barbell formed. Many carry residual loyalty to middle brands that no longer serve them well — yet are treated as afterthoughts by a digital-first world despite controlling the largest share of consumer wealth. The gray-wave wealth transfer is a generational-equity moment most brands are missing.

Strategic implications for brands.

Choose your pole — and commit.

There is no reward for positioning in the middle. The worst strategic position is expensive-but-undifferentiated: paying premium costs to deliver commodity experiences. Pick prestige or pick commodity, and run it without apology.

Premium requires generational equity, not just price.

The prestige pole is maintained by consistent delivery of identity-affirming experiences across decades and cohorts. A high price with no underlying craft is a clearance event waiting to happen.

The commodity pole has its own discipline.

Radical value requires supply-chain mastery, ruthless margin management, and the discipline to resist mission creep. The brands that win at the bottom know exactly what they are — and never pretend otherwise.

Aggregators are not your distribution partners.

They are your competitors for customer relationship. Brands that build primary discovery on third-party platforms are renting access to their own customers and surrendering equity on every transaction.

Each generation reads the barbell differently.

Gen Z defaults to commodity until they invest in identity; Millennials watched the middle promise break; Gen X remembers craft and rewards what they can verify; Boomers carry residual loyalty the digital-first world treats as an afterthought. A unified strategy that ignores generational equity is flying blind.

Why the middle mattered — and what we lost with it.

The disappearing middle is not just a market-structure story. It is a generational-equity story. The mid-tier brand was the commercial equivalent of the journeyman layer — the place where craft developed, standards were maintained, and the relationship between producer and consumer was more than a transaction.

When the guild systems broke and industrial factories took over, we lost the container that made craft transmissible across generations. The factory worker had no standing, no lineage, no identity beyond output. The barbell economy is running the same play again — this time faster and at digital scale, with AI accelerating the commoditization of undifferentiated work at every level.

For brands, institutions, and policymakers, the synthesis is uncomfortable: the barbell is not reversible through nostalgia or incremental improvement. It requires a deliberate answer to the question the middle never had to ask — what do we actually stand for, and is it worth paying for?

Share Your Voice

Join the conversation to share your thoughts and help others understand this topic better.

Join the ConversationCommunity Feedback

No comments yet. Be the first to share your thoughts!