The System Nobody Fixed

A report on the structural failure of American healthcare — documented across physician shortages, rural collapse, long-term care, mental health, and cost.

Every generation eventually discovers the shape of the world it actually inherited, as opposed to the one it was promised. For Americans currently navigating the healthcare system — as patients, as caregivers, as workers, as payers — that discovery is arriving with unusual clarity. The system is not merely stressed. It is failing across multiple dimensions simultaneously, and the failures are not coincidental. They are the predictable consequences of specific policy choices, made and not made, over the past three decades.

This report documents those failures with precision. It does not traffic in alarm for its own sake. The numbers are alarming enough on their own terms.

Part One: The Physician Shortage Is Already Here

The standard way to discuss the American physician shortage is in the future tense — a looming crisis, a coming shortage, a projected deficit. That framing is now inaccurate. The shortage is present tense.

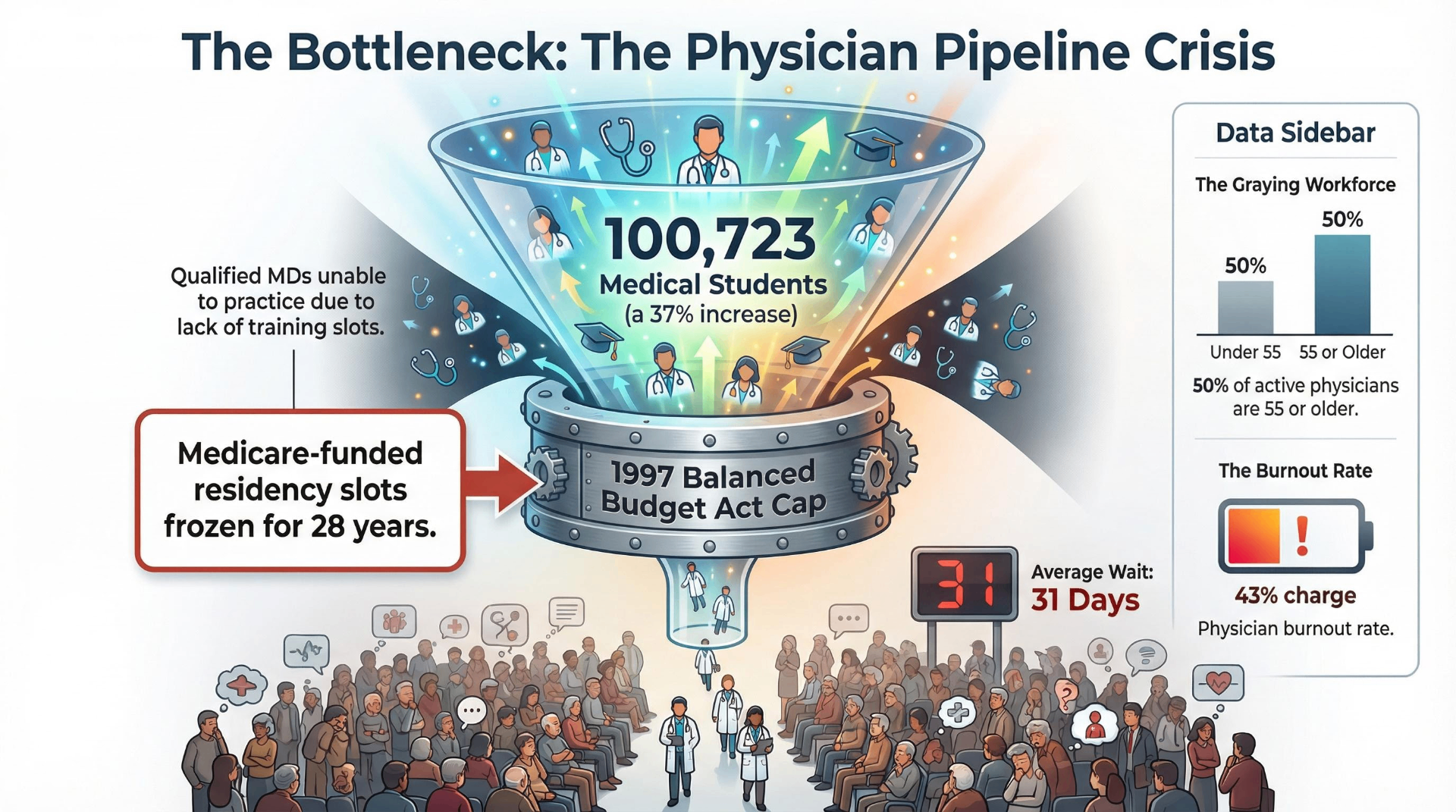

As of 2025, the Health Resources and Services Administration (HRSA) designates 8,467 primary care Health Professional Shortage Areas (HPSAs) in the United States, covering 92.3 million Americans. That is a 9.7% increase in the number of shortage areas from just one year prior. Roughly 48% of primary care need is currently being met in those areas. An additional 15,604 practitioners would be needed simply to eliminate the existing shortage designations — not to achieve ideal coverage, but to reach the threshold at which HRSA stops formally classifying a community as underserved.

The Association of American Medical Colleges (AAMC) projects a total physician shortfall of 13,500 to 86,000 physicians by 2036, with primary care specifically facing a gap of 20,200 to 40,400. HRSA's own modeling is more severe: a projected shortage of 68,020 primary care full-time equivalents by 2036, and 187,130 total physician FTEs by 2037. The range between these projections reflects genuine modeling uncertainty. Both directions point the same way.

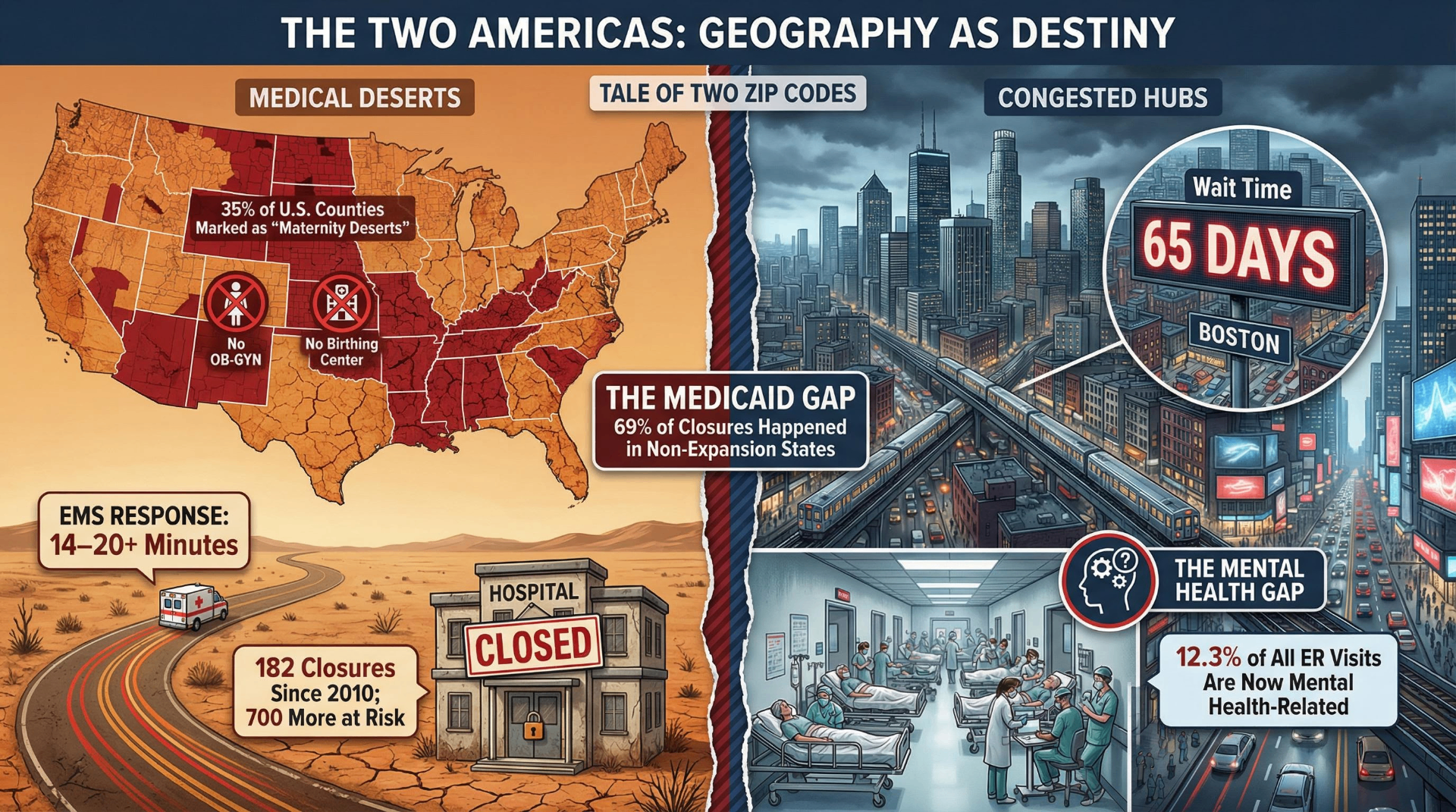

The wait time data translates projections into lived experience. The average time for a new patient to see a physician now stands at 31 days across major metropolitan areas — a 48% increase since 2004 and a 19% increase since 2022 alone, according to AMN Healthcare's 2025 survey. In Boston, the average is 65 days. For family medicine specifically, the average is 23.5 days and rising. The result is measurable and economically significant: an estimated 65% of Americans report they would use an emergency room if they could not get a timely physician appointment — at costs up to twelve times higher than an office visit.

The structural cause is well understood and rarely disputed. In 1997, the Balanced Budget Act capped Medicare-funded residency positions at each hospital's 1996 count. The cap was based on then-prevailing projections that the U.S. was producing too many physicians — projections that proved to be incorrect. Medicare currently spends approximately $21.2 billion annually supporting 124,034 full-time resident physicians, and that number has not meaningfully grown in 28 years. Medical schools, recognizing the demand, have expanded enrollment — reaching 100,723 students in 2025-26, a 37% increase over two decades. But enrollment growth without residency slot growth produces physicians who complete four years of medical school and cannot complete their training. The pipeline has a bottleneck, and the bottleneck was installed by law.

The first modification to the cap came in 2021, when the Consolidated Appropriations Act added 1,000 new Medicare-supported positions — 200 per year over five years. This was the first increase in 23 years. The Resident Physician Shortage Reduction Act, reintroduced in 2025, would add 14,000 positions over seven years. It has failed to pass in multiple prior congressional sessions.

Meanwhile, the physician workforce is aging faster than it is being replaced. Approximately 25% of active physicians are 65 or older, and another 25% are between 55 and 64. More than a third of the current workforce will reach retirement age within a decade. The American Medical Association reports physician burnout at 43.2% in 2024 — down from a pandemic peak of 62.8% but still 82% higher than burnout rates among comparably educated non-physician workers. The Commonwealth Fund reports that more than one-third of burned-out primary care physicians plan to stop seeing patients within one to three years. The retirement wave and the burnout-driven exodus are arriving simultaneously.

Part Two: Geography as Medical Destiny

The physician shortage is not uniformly distributed. Its most severe expression is geographic, and its consequences are most acute for the approximately 60 million Americans who live in rural communities.

The Chartis Center for Rural Health's 2025 State of the State report documents 182 rural hospital closures or conversions since 2010. Another 432 rural hospitals are currently classified as vulnerable, with 46% operating at negative financial margins. The Center for Healthcare Quality and Payment Reform estimates that over 700 rural facilities face some risk of closure, with 315 in imminent financial danger. The most exposed states — Texas (47 vulnerable hospitals), Kansas (46), Mississippi (28) — are disproportionately those that have not expanded Medicaid under the Affordable Care Act.

That connection is not incidental. 69% of rural hospital closures between 2014 and 2024 occurred in states that had not expanded Medicaid. Rural hospitals in expansion states are 62% less likely to close than those in non-expansion states, and their uncompensated care burden — the cost of treating patients who cannot pay — runs at 2.55% of operating expenses versus 6.28% in non-expansion states. Ten states still have not expanded Medicaid. All ten rank among the worst in the country for rural hospital financial stability.

The specialties most concentrated in urban centers produce their own form of geographic inequality. The March of Dimes' 2024 report documents that 35% of U.S. counties — 1,104 in total — are maternity care deserts, with no birthing facility and no obstetric clinician. 5.5 million women live in these counties. The consequences are measurable: maternal mortality in the most rural counties is 1.6 times higher than in large metropolitan counties.

The rural-urban gap extends across virtually every health metric. All ten leading causes of death carry higher rates in rural areas than urban ones. Heart disease mortality is 21% higher; cancer 15% higher; chronic lower respiratory disease 48% higher. The age-adjusted mortality rate for prime working-age adults — those between 25 and 54 — was 43% higher in rural areas in 2019 than in urban areas, a gap that barely existed 25 years earlier. EMS response times in rural communities average over 14 minutes — double the national average — with a 2025 American College of Surgeons study finding rural response times nearly 20 minutes longer than average for high-acuity calls.

HRSA projects that by 2038, nonmetropolitan areas will experience a 58% physician shortage compared to 5% in metropolitan areas. These are not projections about the distant future. Given the current trajectory of rural hospital closures, the physician retirement wave, and the geographic concentration of residency programs, the 2038 projection is arguably conservative.

Part Three: The Nursing Home Mandate That Lasted Twenty Months

In April 2024, the Centers for Medicare and Medicaid Services issued the first-ever federal minimum staffing standards for long-term care facilities. The rule required 3.48 hours of nursing care per resident per day, including at least 0.55 hours from a registered nurse and 2.45 from a nurse aide, and mandated a registered nurse on-site around the clock. Researchers at the University of Pennsylvania estimated the rule would prevent approximately 13,000 nursing home deaths per year.

The compliance picture revealed the depth of the problem. KFF analysis found that only 19% of nursing facilities met all three staffing minimums under the rule as written. The industry trade association AHCA estimated only 6% met all four requirements including the 24/7 RN mandate. Full compliance would have required roughly 102,000 additional workers at an estimated annual cost of $6.5 billion.

On December 2, 2025 — twenty months after issuance — CMS repealed the rule. Staffing requirements reverted to the previous standard: a registered nurse on-site for only eight consecutive hours per day. The stated rationale cited workforce availability constraints and administrative flexibility for rural facilities. The Medicare Rights Center responded that the rollback would leave nursing home residents less safe. The Federal Register notice offered no projection of how many deaths the repeal might be expected to cause.

The underlying workforce reality that made compliance difficult is real. The U.S. nursing workforce has been in structural decline since the COVID-19 pandemic triggered an exodus of experienced nurses. Approximately 100,000 registered nurses left the workforce during COVID. HRSA projects an 8% RN shortage in 2028, with nonmetropolitan areas facing deficits roughly 2.6 times more severe than metropolitan ones. Over 1 million nurses are projected to retire by 2030.

The pipeline cannot compensate. In 2024, 80,162 qualified applicants were turned away from nursing programs — not for lack of academic qualification, but for lack of faculty and clinical placement capacity. There are 1,588 open full-time faculty positions in nursing schools nationally, and average nursing faculty salaries of $84,000 cannot compete with clinical nurse salaries that regularly exceed $125,000. The average age of active nurses is 46, with more than 50% aged 50 or older.

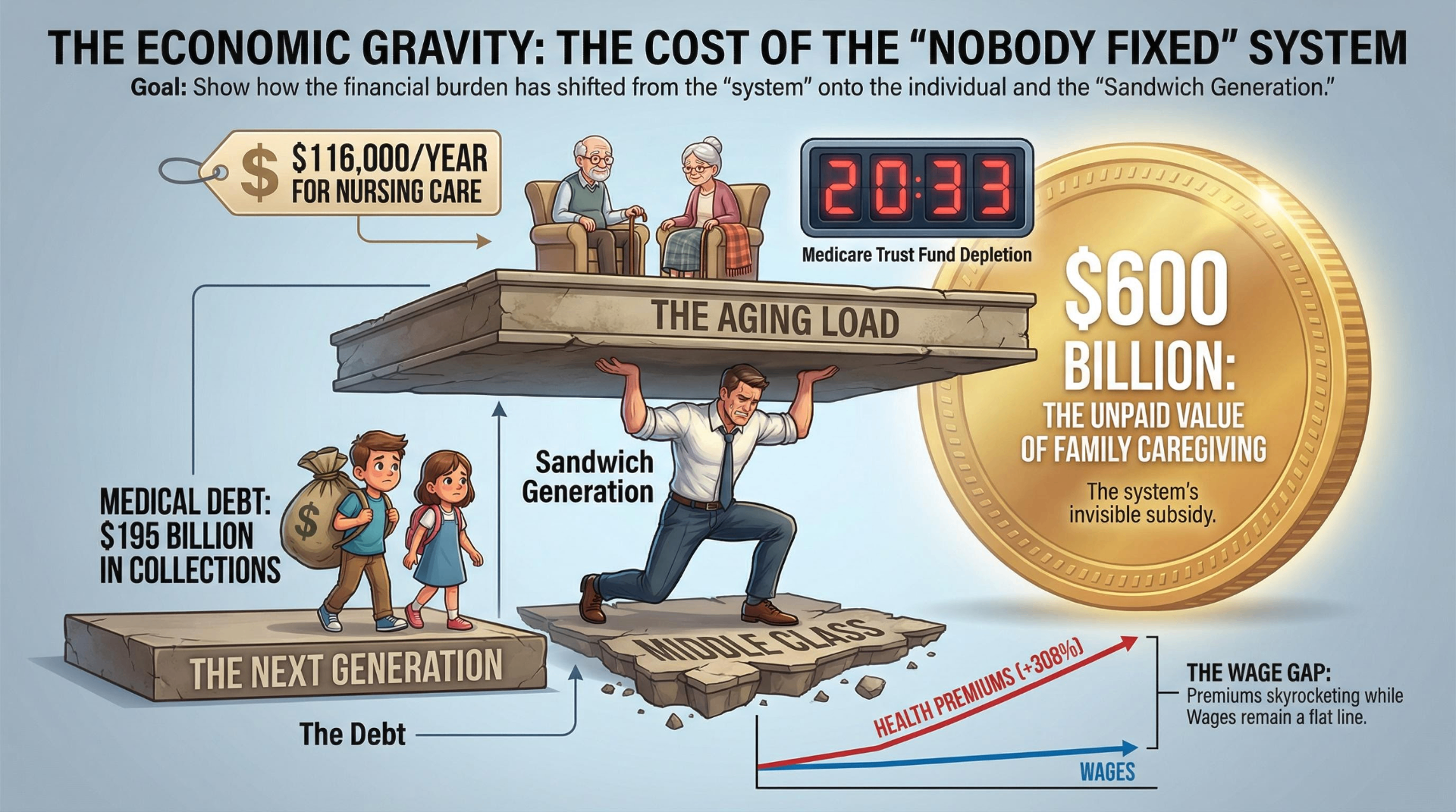

The aggregate picture in long-term care is one of compounding failures. Demand is accelerating: the population aged 85 and older is expected to more than double by 2040, from 6.7 million to 14.4 million. Nursing home costs have reached a median of $116,000 per year for a private room. 70% of Americans will require some form of long-term care, but only 7% have long-term care insurance. Medicare covers a maximum of 100 days of skilled nursing care following a qualifying hospital stay. After that, costs are borne by the patient, their family, or Medicaid — for those who qualify.

Nearly 1 in 4 American adults now identifies as part of the sandwich generation, providing care for both children and aging parents. On average, these caregivers spend 50 hours per week on caregiving activities — equivalent to a full-time job — while 47% report being unable to meet essential household expenses due to caregiving costs. The unpaid family caregiving labor that props up the formal care system is valued at over $600 billion annually. It does not appear in GDP calculations, does not generate Social Security credits, and receives no direct policy support at the federal level.

Part Four: The Mental Health System That Never Was

The United States does not have a mental health system in any meaningful sense of the term. It has a collection of inadequately funded, inadequately staffed, and inadequately insured services that collectively meet roughly 27% of national mental health need, according to HRSA's December 2025 designation data.

137.1 million Americans — more than 40% of the total population — live in designated mental health Health Professional Shortage Areas. There are approximately 51,000 practicing psychiatrists in the country; 60% are 55 or older, meaning the majority of the existing workforce is approaching retirement. 65% of rural counties and 50% of all U.S. counties have no practicing psychiatrist at all. HRSA projects a national shortage of 43,660 adult psychiatrists by 2038.

The child and adolescent psychiatry numbers are worse. Only approximately 11,400 child and adolescent psychiatrists practice in the country, with 72% of counties having none. SAMHSA estimates the U.S. needs at least 48,000 to 49,000 additional child psychiatrists to meet children's treatment needs. The average delay between a child's first mental health symptoms and receiving treatment is 11 years.

The practical consequence of this shortage is that emergency departments have become the default mental health intake system. 12.3% of all adult emergency department visits are mental health-related, and among youth, the proportion of ED visits attributable to mental health approximately doubled between 2011 and 2020. Psychiatric emergency visits are four times more likely to result in extended boarding — patients waiting in emergency hallways for psychiatric placement — than non-psychiatric visits. In some states, children admitted for psychiatric crisis wait an average of more than 24 hours in the emergency department before placement. This is not a gap in service. It is the service.

Insurance does not adequately cover mental health care even when providers are available. Patients go out-of-network 3.5 times more often for behavioral health than medical or surgical care, and 8.9 times more often specifically for psychiatrists. Reimbursement rates for behavioral health clinicians run 22% lower than for medical and surgical clinicians of comparable training. The Mental Health Parity and Addiction Equity Act requires insurance coverage for mental health to be equivalent to coverage for physical health. In May 2025, the federal government announced it would not enforce the 2024 final rule that would have strengthened parity requirements.

Telehealth has provided partial mitigation. Behavioral health telehealth visits grew from approximately 1% of claims pre-pandemic to a majority of behavioral health appointments by 2024. But 596 U.S. counties lack both psychiatrists and broadband internet access, rendering telehealth solutions irrelevant for approximately 10.5 million residents. The access problem in these communities is not a technology problem. It is a fundamental absence of service.

Part Five: The Cost of a System That Doesn't Reach You

American healthcare spending reached $5.3 trillion in 2024, equal to $15,474 per person — an 18% share of GDP that is projected to rise to 20.3% by 2033, according to CMS national health expenditure projections. The United States spends approximately 88% more per capita on healthcare than comparable wealthy nations and delivers results that consistently rank last among high-income countries on access, equity, and efficiency measures (Commonwealth Fund Mirror, Mirror 2021).

The cost distribution is not abstract. Average employer-sponsored family premiums reached $26,993 in 2025, having grown approximately 6-7% annually in recent years. Worker contributions toward those premiums increased 308% between 1999 and 2024. Average deductibles have tripled since 2006, from $584 to $1,886. In 37 states, combined premium contributions and deductibles consumed more than 10% of median household income. A 2025 survey of insured adults found 38% had delayed or skipped needed care due to cost — a 41% increase from 2023 — with 42% reporting their condition worsened as a result.

The Medicare program that finances coverage for the 66 million Americans aged 65 and older is approaching a structural crisis of its own. The 2025 Medicare Trustees Report, issued June 2025, moved the Hospital Insurance Trust Fund depletion date to 2033 — three years earlier than the prior year's projection. At depletion, revenues are projected to cover only 89% of scheduled Part A benefits, meaning an automatic 11% benefit cut without legislative action. Medicare costs are currently 3.8% of GDP and projected to reach 6.2% by 2049.

The Medicaid program — which covers 75.7 million low-income Americans and finances a substantial portion of long-term care — faces a different kind of structural pressure. The One Big Beautiful Bill Act, signed July 4, 2025, enacted Medicaid reductions estimated at $911 billion to $1.06 trillion over ten years. The Congressional Budget Office projects 7.5 million people will lose Medicaid coverage, and combined with expiring ACA enhanced subsidies, approximately 15 million Americans are projected to be uninsured by 2034 who would otherwise have had coverage. Rural hospitals, disproportionately dependent on Medicaid reimbursement, face projected reimbursement declines of 21% under the bill's provisions.

Medical debt sits at the intersection of inadequate coverage and inadequate access. An estimated 36–41% of U.S. adults carry medical debt, with approximately $194–195 billion currently in collections — 58% of all debt in collections, more than any other category. In 2024, roughly 31 million Americans borrowed an estimated $74 billion to pay for healthcare.

Part Six: What Policy Would Fix

The healthcare crisis is documented in considerable detail. It is less frequently acknowledged that the structural solutions are also documented in considerable detail — and that most of them have existed in legislative draft form for years without passing.

Lifting the Medicare GME cap and adding 14,000 residency positions over seven years would directly address the physician shortage pipeline. The legislation is bipartisan, endorsed by every major medical association and hospital organization, and estimated to cost approximately $10 billion over 10 years — a fraction of what physician shortages cost in emergency utilization and deferred care. It has not passed.

Universal Medicaid expansion to the remaining 10 holdout states would immediately address a substantial portion of rural hospital financial instability. The federal government covers 90% of expansion costs. The 10 non-expansion states collectively have the highest rates of rural hospital closure and the worst rural health outcomes in the country. They have not expanded.

Federal minimum nursing home staffing standards would reduce preventable deaths in the country's most vulnerable care settings. The rule was issued, survived legal challenge, and was voluntarily rescinded before its compliance deadlines took effect.

Mental health parity enforcement would require that insurance coverage actually reflect the legal requirements already on the books. The 2024 final rule was not enforced.

None of these represent novel or untested policy. They represent the application of resources, enforcement authority, and legislative will to problems whose dimensions are precisely understood. The question the data does not answer — and that each generation will have to answer for itself — is why a system this thoroughly documented in its failures has proven this resistant to repair.

Conclusion: The Inheritance

The healthcare crisis is not a future event. It is a present condition distributed unevenly across geography, income, and age — but expanding its reach in all directions. The physician shortage is measured in current HPSAs covering 92 million people. The rural hospital crisis is measured in current closures and current vulnerable facilities. The long-term care shortage is measured in current staffing ratios and current care costs. The Medicare insolvency is measured in a trust fund depletion date now eight years away.

Each generation experiences the same system differently but is shaped by it regardless. Baby Boomers, the largest demand driver in the history of American healthcare, are arriving at their highest-need years as the geriatrician supply is smaller than it was in 2000. Gen X is performing the unpaid labor of caregiving for those Boomers while absorbing their own costs in a system with fewer specialists, higher premiums, and more constrained access than the one their parents used. Millennials carry more medical debt as a cohort than any prior generation and are less likely to have a primary care physician. Gen Z is entering adulthood into a mental health system that functionally does not exist and inheriting the fiscal consequences of decisions made before they could vote.

What distinguishes this crisis from most is not its complexity. It is the clarity with which the structural causes are understood, the availability of documented interventions, and the persistence of the gap between what is known and what has been done.

The system was not broken by neglect alone. It was shaped by choices. It will only be repaired by different ones.

Between Silicon and Soul explores the technology, policy, and cultural forces reshaping generational life. This report is part of the Healthcare & Systems series.

Share Your Voice

Join the conversation to share your thoughts and help others understand this topic better.

Join the ConversationCommunity Feedback

No comments yet. Be the first to share your thoughts!