The Molecule That Ate Everything

GLP-1 drugs as society's mirror — a research synthesis on generational identity, class dynamics, and the architecture of American capitalism.

GLP-1 receptor agonists have become the most culturally significant pharmaceutical class since the birth control pill. What began as a diabetes treatment has metastasized into a $62–70 billion global market reshaping generational identity, class dynamics, and the architecture of American capitalism. Approximately 12% of U.S. adults — roughly 40 million people — have now used a GLP-1 drug for weight loss, with prescriptions surging 587% between 2019 and 2024.

But behind the transformation photos and stock price explosions lies a more complex story: one about who gets to be thin, what technology promises versus what it delivers, and whether a weekly injection can paper over the structural rot of the American food system.

I. The Generational Fault Line: Who's Injecting and Why It Matters

Gen X owns the needle; Gen Z is reimagining the concept

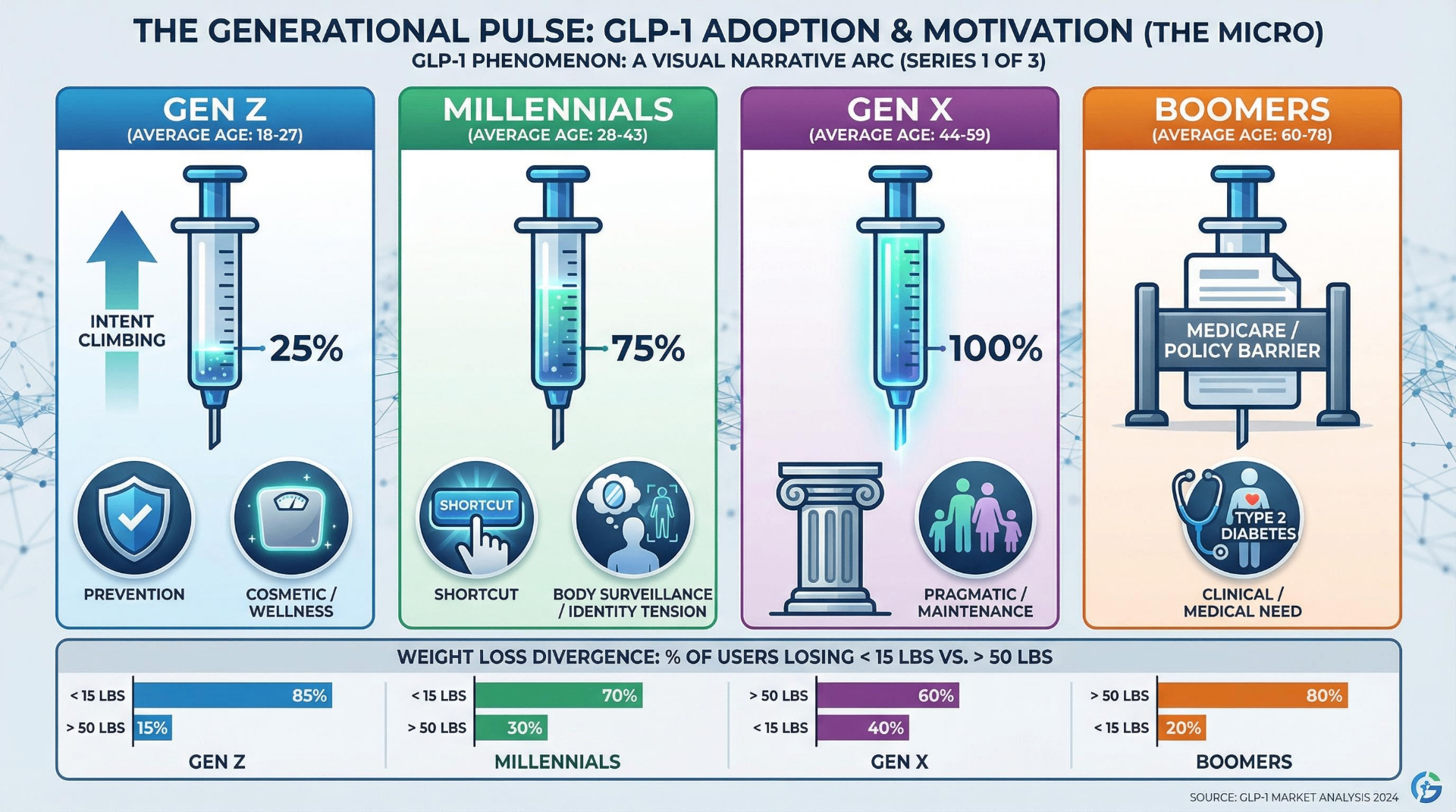

The demographic profile of the typical GLP-1 user defies easy assumptions. Gen X is the dominant cohort, comprising 35% of all users despite representing just 25% of the adult population. Millennials over-index at 31%. Boomers and Gen Z are underrepresented in current usage — but for entirely different reasons. Morning Consult's massive February 2026 survey (n=58,008) reveals the archetypal user: married, urban, children at home, household income above $100,000 (2.2× overrepresentation), master's degree or higher (2.25× overrepresentation), and insured (96% versus 86% general population).

But growth tells the more interesting story. Evernorth's data shows GLP-1 use among Gen Z surged 177.7% year-over-year and 67.8% cumulatively from 2023–2024. Gen Alpha (ages ≤14) saw an 84.6% increase. A Tebra survey found 37% of Gen Z plans to incorporate GLP-1s into their 2025 wellness goals — the highest intent of any generation. This is the "injection native" generation: they didn't spend decades failing at diets before discovering semaglutide. They're approaching it as prevention, not remediation.

The generational psychology diverges sharply. Numerator's analysis of 100,000+ panelists found 60% of those using GLP-1s for diabetes management are Boomers, while Gen Z users are 5× more likely to use them for weight management than diabetes. A striking 42% of users trying to lose fewer than 15 pounds are Millennials or Gen Z — suggesting cosmetic and wellness-driven adoption rather than clinical need. Millennials are the most likely to know someone using GLP-1s (41%) and paradoxically the most likely to label them a "shortcut" (77%), yet they adopt anyway. Gen X, the pragmatic sandwich generation in peak earning years, is the least likely to accept the shortcut framing (33%).

Boomers face a unique structural barrier: Medicare's statutory exclusion of weight-loss drugs, dating to a 2003 law passed in the fen-phen aftermath. Only 1% of adults 65+ have taken GLP-1s for weight loss despite 37% being told by doctors they're overweight. This is beginning to change — the November 2025 Trump administration deal with Novo Nordisk and Eli Lilly brings Medicare pricing to $245/month with a $50 copay, and a Medicare GLP-1 Bridge program launches in July 2026 — but the generational gap in access has already calcified into years of divergent health trajectories.

Social media turned a drug into an identity

GLP-1 culture is inseparable from the platforms that amplify it. A Basch et al. study published in the Journal of Medicine, Surgery, and Public Health found that just 100 TikTok videos under #Ozempic accumulated 69.9 million views, with 57% discussing weight-loss use and over one-third explicitly encouraging others to try it. Less than 5% mentioned off-label risks, medication shortages, or alternatives. On Instagram, 306,000 posts carry #ozempic and 301,000 carry #semaglutide, with 80% created by personal users rather than healthcare professionals. A Springer Nature analysis found gastrointestinal side effects — the most common clinical adverse effect — were essentially invisible on Instagram.

Morning Consult's 2026 data reveals GLP-1 users dramatically over-index on every social platform: +32 percentage points on TikTok (68% vs. 36% of all adults), +21 on Instagram, +22 on Reddit. These users self-identify as early adopters (+15 pp), trend seekers (+15 pp), and status-driven (+12 pp). They also over-index on luxury brand interest: Rolex (+25.4 pp), Mercedes-Benz (+25.3 pp), Royal Caribbean (+26.8 pp). GLP-1 adoption correlates with a specific socioeconomic and cultural identity, not merely a medical need.

The celebrity disclosure ecosystem has become its own cultural text. Oprah Winfrey revealed, then quit, then resumed GLP-1 use; Elon Musk publicly switched from Wegovy to Mounjaro; Nikki Glaser declared on the Tonight Show that "the shame is only from thin people who want you to stay fat." Lizzo — perhaps the most symbolically loaded figure in this conversation — initially denied using GLP-1s, then admitted it on a podcast in June 2025: "I tried everything." She was parodied on South Park and later reclaimed the narrative by dressing as "LizzOzempic" for Halloween.

The Harvard Petrie-Flom Center called the celebrity-Ozempic discourse "a regulatory nightmare", noting the FDA's social media drug marketing guidance was last updated in 2014 — before TikTok existed and when Instagram was three years old.

Body positivity meets its pharmaceutical antagonist

The collision between the body positivity movement and GLP-1 culture may be the most revealing cultural tension of the decade. TIME's 2023 assessment was blunt: "The Ozempic craze is a swift wind that has revealed that we've spent the past decade building a house of cards." The modern body positivity movement, critics argue, diluted its political roots in 1960s fat Black women's activism into shallow "self-love" messaging that couldn't withstand a genuinely effective weight-loss drug.

A 2025 Rutgers University study in the journal Body Image found participants most interested in GLP-1s reported greater body shame, body surveillance, weight concerns, anti-fat bias, and disordered eating behaviors. Body appreciation acted as a protective moderator against GLP-1 interest. A randomized study found a woman who lost weight via GLP-1 was judged more negatively than one who lost the same amount through diet and exercise — the "shortcut penalty." Yet 56% of Gen Z says GLP-1 popularity negatively impacts their self-image, even as 37% plan to use the drugs. This is a generation at war with itself.

The "food noise" revolution and its psychological shadow

The concept of "food noise" — the constant, intrusive mental preoccupation with food decisions — has emerged as perhaps the most paradigm-shifting element of GLP-1 therapy. One patient told Scientific American: "All of a sudden it was like some part of my brain that was always there just went quiet. It felt almost surreal to put an injector against my leg and have happen in 48 hours what decades of intervention could not accomplish." Data presented at the EASD 2025 meeting showed 64% reported improved mental health, 76% improved self-confidence, and 80% healthier habits.

The neurological implications extend beyond food. A 2025 JAMA Psychiatry study found semaglutide reduced alcohol cravings; a Nature Medicine study of 2 million+ patients showed reduced risk of substance addiction to alcohol, cannabis, opioids, and stimulants. GLP-1s appear to broadly modulate the brain's reward circuitry, raising profound questions about pharmaceutical manipulation of desire itself.

But the psychological shadow is real. A 2024 Scientific Reports study found GLP-1 users with obesity had nearly double the risk of major depression versus control groups. An April 2025 research article suggested GLP-1s may drive depression and suicidal ideation in people with genetic predisposition toward low dopamine function. Australia's TGA aligned product warnings across all GLP-1 agonists in June 2025: "Suicidal behaviour and ideation have been reported." The counterevidence is substantial — Mendelian randomization studies found no causal link, and Novo Nordisk–funded trials showed small reductions in depressive symptoms — but the signal persists in pharmacovigilance data. The FDA FAERS database documents psychiatric reactions at approximately 1.2% of all GLP-1 reports.

Eating disorder specialists are alarmed. The Academy for Eating Disorders warns younger individuals are particularly susceptible. Dr. Cynthia Bulik, a leading eating disorder researcher, cautioned: "Focus on weight and erasing the desire to eat could indeed do harm." When appetite suppression is so complete that eating feels impossible, GLP-1 therapy can "mimic and reinforce patterns seen in anorexia nervosa." One user described GLP-1s as "doctor-approved anorexia" — a gray zone that complicates clinical assessment of eating-disorder risk.

II. Where Silicon Meets Semaglutide: AI, Telehealth, and the Drug Pipeline

Telehealth platforms turned prescriptions into subscriptions

The GLP-1 boom created a new category of digital health company. Hims & Hers reached 2.44 million subscribers by Q2 2025 (up 31% year-over-year), generating $536.9 million in quarterly online revenue (up 75%). Ro launched its Body Program at $145/month membership plus medication. Noom expanded into GLP-1 prescribing while maintaining its behavioral platform, claiming users lose 48% more weight with Noom Med versus medication alone.

In April 2025, Novo Nordisk partnered directly with Hims & Hers, Ro, and LifeMD to deliver branded Wegovy at $499/month cash price via NovoCare Pharmacy. But the partnership with Hims collapsed spectacularly: Novo terminated it in June 2025, citing "illegal mass compounding" and "deceptive marketing," sending Hims stock down 34%. When Hims launched a compounded oral semaglutide pill in February 2026 at $49 for the first month, HHS referred the company to the DOJ, and Novo sued for patent infringement. Hims pulled the product within days.

WeightWatchers' trajectory is the starkest cautionary tale. After acquiring telehealth platform Sequence for $132 million in March 2023 to prescribe GLP-1s, the 62-year-old company filed Chapter 11 bankruptcy in May 2025 with $1.6 billion in debt. It emerged 42 days later as a private company after eliminating $1.15 billion in obligations. The company that once defined American dieting was rendered obsolete by a molecule.

The compounding pharmacy war exposed the gray market's scale

When FDA added Ozempic and Wegovy to its drug shortage list in 2022, compounding pharmacies rushed to fill the gap, creating an enormous gray market for cheaper semaglutide copies. As of early 2026, Novo Nordisk estimated 1.5 million Americans were using compounded GLP-1s. But safety data was alarming: FDA FAERS data documented 442 adverse event cases with compounded semaglutide, including 319 classified as "serious," 99 hospitalizations, and 7 deaths. Novo Nordisk's own testing found some compounded products contained no semaglutide at all, while others had up to 86% impurities.

The legal crackdown was methodical. By August 2025, Novo Nordisk had filed 132 lawsuits across 40 states, obtaining 44 permanent injunctions. FDA declared the semaglutide shortage resolved in February 2025 and ended enforcement discretion for compounding by May 2025. The compounding era is effectively over — but it revealed both the desperation of patients priced out of branded drugs and the regulatory infrastructure's inability to keep pace with demand.

AI is redesigning the molecules themselves

The most consequential AI intersection isn't in prescribing — it's in drug discovery. Insilico Medicine used its Biology42 engine to generate 5,000+ novel peptides targeting the GLP-1 receptor in just 72 hours; 14 of 20 tested showed biological activity, with 3 achieving single-digit nanomolar potency — a level typically requiring multiple design iterations over months. The company has advanced two oral GLP-1 receptor agonists and an amylin receptor agonist to preclinical candidate stage, with IND-enabling studies underway.

Broader AI drug discovery is accelerating the metabolic medicine pipeline. Recursion merged with Exscientia in 2024, creating an end-to-end AI platform combining phenomic screening with automated precision chemistry. Sanofi committed $1.2 billion to an AI-driven discovery partnership. The earliest AI-discovered metabolic drug approval is estimated for 2029–2031, though AI is compressing traditional development timelines significantly.

The next-gen pipeline promises to rewrite the weight-loss ceiling

The drugs currently in development make today's semaglutide look like a warm-up act:

Retatrutide (Eli Lilly), a triple agonist targeting GLP-1, GIP, and glucagon receptors simultaneously, delivered 28.7% mean weight loss (71 pounds average) at 68 weeks in the TRIUMPH-4 trial — some participants stopped due to "perceived excessive weight loss." Regulatory submission is expected in 2026 with potential approval in late 2027.

CagriSema (Novo Nordisk), combining semaglutide with the amylin analog cagrilintide, achieved 22.7% weight loss in the REDEFINE-1 trial published in NEJM June 2025, with 23% of participants losing ≥30% of body weight. NDA filed December 2025.

Orforglipron (Eli Lilly), an oral non-peptide GLP-1 agonist requiring no fasting restrictions, showed 12.4% weight loss over 72 weeks with potentially easier and cheaper manufacturing. FDA decision expected mid-2026.

Oral Wegovy (25mg semaglutide pill), approved December 22, 2025, achieved 16.6% weight loss and launched at $149/month — removing the injection barrier that 50% of potential users cited as their primary obstacle.

Wegovy HD (7.2mg injection), approved March 19, 2026, achieved 20.7% mean weight loss in just 54 days of FDA review under the new National Priority Voucher program.

Beyond these, MariTide (Amgen) promises monthly or less-frequent dosing; VK2735 (Viking Therapeutics) showed 12% weight loss in Phase 2 as an oral dual agonist; and mazdutide (Innovent Biologics, China) demonstrated superiority over semaglutide in a head-to-head Phase 3 trial. Over 60 companies are developing GLP-1 drugs globally, with more than 135 candidates in clinical trials.

Wearables, CGMs, and the data layer

The August 2025 FDA clearance of Signos — the first CGM-based system specifically approved for weight management — signals the convergence of continuous glucose monitoring with GLP-1 therapy. At $129–139/month, Signos uses Dexcom sensors paired with an AI-powered app for personalized lifestyle recommendations. Research shows 87% of CGM users change food choices based on glucose feedback.

The theoretical endpoint is a digital twin — a personalized metabolic model built from accumulated CGM, wearable, and genomic data that could optimize GLP-1 dosing, predict who will respond best to which drug, and guide eventual discontinuation. This remains largely research-stage, but the data infrastructure is being laid.

Could we eventually escape lifetime dependency?

Current evidence is sobering: GLP-1s require chronic use, and weight rebounds rapidly when stopped. But several converging technologies offer potential escape routes. CRISPR researchers at Harvard's Joslin Diabetes Center converted white fat to brown fat in mouse models, preventing weight gain on high-fat diets. UCSF researchers used CRISPRa to upregulate genes in the hypothalamus, preventing severe obesity without any permanent genome editing. These are all mouse studies — human trials are years away — but they represent fundamentally different approaches: addressing obesity at its genetic roots rather than suppressing appetite pharmacologically.

Microbiome engineering offers another vector. University of Utah researchers identified in December 2025 a specific gut bacterium, Turicibacter, that improves metabolic health and reduces weight gain. The most realistic near-term path, however, isn't elimination of drug dependency but optimization of it: AI helps tailor dosing, CGMs track metabolic response, and behavioral platforms build habits that sustain weight loss during tapering — enabling some patients to discontinue.

III. The Class Divide That a Molecule Made Visible

The arithmetic of exclusion

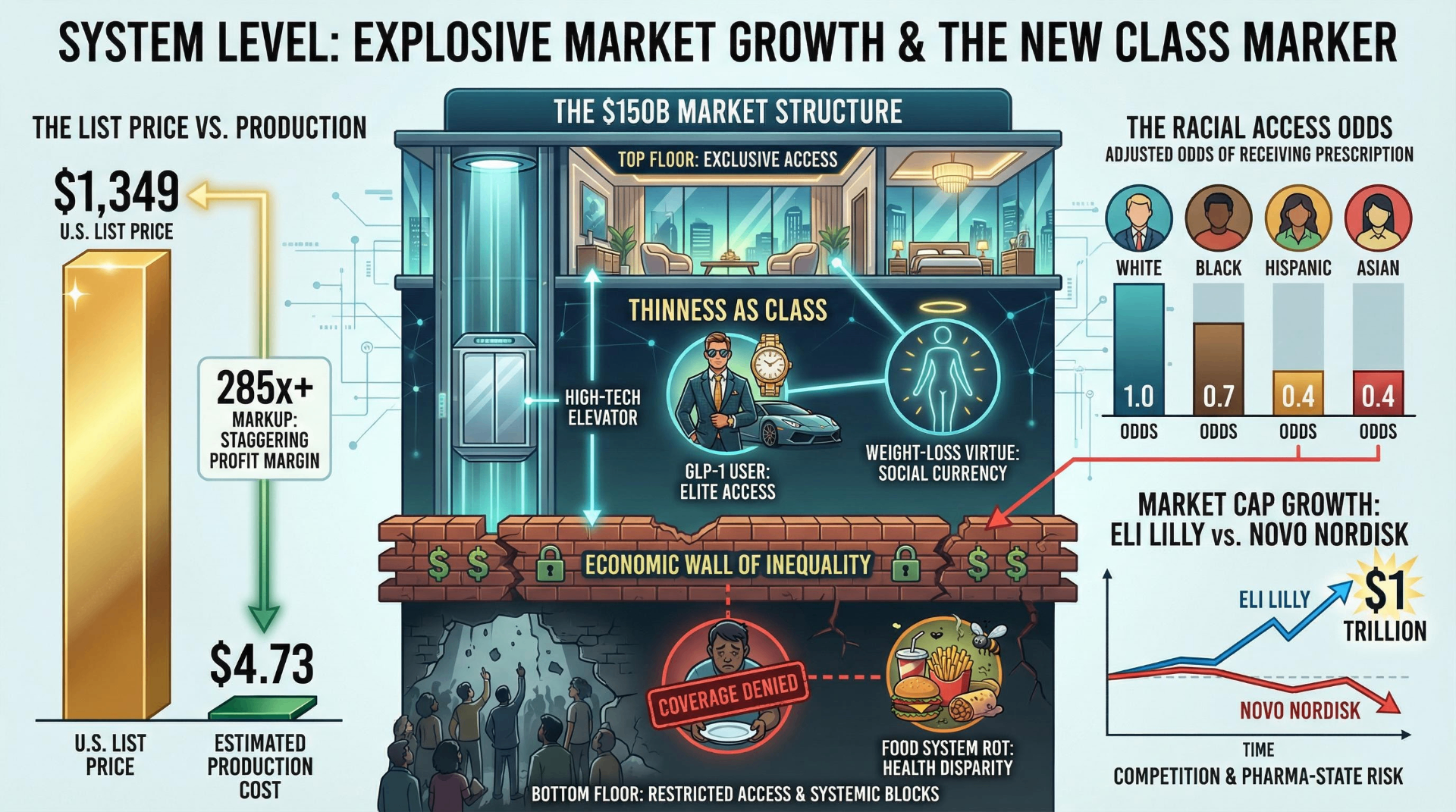

The numbers are stark. Wegovy's list price is $1,349/month. Production cost, per a JAMA Network study, is estimated at $0.89 to $4.73 per month including a reasonable profit margin. That is a markup of roughly 285× to 1,516×. In the UK, the same drug costs $92. In Germany, $137–328. In Canada, $265. The U.S. pays approximately 15 times what the UK pays for identical semaglutide.

The November 2025 Trump-Pharma deal brought meaningful price compression: $245/month for Medicare and Medicaid, $349/month cash-pay through NovoCare, oral Wegovy at $149/month. These are genuine improvements. But even at $149/month ($1,788/year), the annual cost represents 2.4% of median household income — a nontrivial burden for a drug that requires chronic use. States with the highest obesity rates (Mississippi, West Virginia, Louisiana, all exceeding 40% obesity) also have the lowest median incomes, creating maximum economic burden precisely where medical need is greatest.

Insurance coverage remains fragmented. Only 19% of firms with 200+ workers cover GLP-1s for weight loss, though this rises to 43% among firms with 5,000+ employees — another mechanism by which large-employer privilege concentrates access. GLP-1 drug costs consumed 10.5% of total annual insurance claims in 2024, up from 6.9% in 2022.

Racial disparities reveal the system's deepest fracture

The access gap follows America's familiar racial fault lines. A TriNetX study of 57,320 patients found that compared to White patients, adjusted odds of receiving tirzepatide were 0.7 for Black patients, 0.4 for Hispanic patients, and 0.3 for Asian patients. A JAMA Research Letter confirmed fewer than 3% of eligible people with obesity receive GLP-1 prescriptions at all — and within that small pool, Hispanic patients receive them at just 1.8% versus 2.4% for non-Hispanic White patients. A JAMA Health Forum study found 40% of all GLP-1 prescriptions went unfilled, with Black patients at a 55.3% fill rate versus 60.9% for White patients.

These disparities overlay onto a population where obesity disproportionately affects Black and Hispanic communities, who are simultaneously least able to afford treatment. A county-level analysis found the highest off-label prescribing rate (51.6%) in Hawaiian counties with median income $92,124; the lowest (31.2%) in American Indian reservation counties with median income $52,437.

Thinness as the new class marker

An MDPI/Nutrients journal analysis stated it plainly: GLP-1 receptor agonists risk "entrenching a two-tiered system in which affluent or well-insured individuals access advanced pharmacological weight loss treatments, while disadvantaged groups remain excluded... This raises the critical question of whether GLP-1RAs are becoming 'treatments only for the rich.'"

The data supports the thesis. Morning Consult found GLP-1 users over-index heavily on luxury consumption: Rolex (+25.4 pp), Mercedes-Benz (+25.3 pp), Royal Caribbean (+26.8 pp). Cornell found GLP-1 households reduce grocery spending by 5.3% overall, but 8.2% among higher-income households. A PMC narrative review concluded that while GLP-1s may reduce stigma by medicalizing obesity, disparities in access "may inflate existing biases against those who cannot afford treatment." The cruel paradox: a drug that could de-moralize obesity may instead create a new moral hierarchy based on who can afford pharmaceutical thinness.

The discontinuation cliff is the cruelest economics

The weight-regain data constitutes the economic time bomb at the heart of GLP-1 therapy. Half of patients stop within one year; 70% within two years (UAB Comprehensive Diabetes Center). The STEP 1 trial extension found participants regained two-thirds of weight loss after stopping semaglutide. A University of Oxford study published in the BMJ in January 2026 projected weight would return to pre-treatment levels within approximately 1.7 years of discontinuation, with cardiovascular improvements reversing within 1.4 years. A March 2026 study found that stopping GLP-1s raises the risk of heart attack, stroke, and death.

The primary reason for discontinuation is cost and insurance coverage limitations — not side effects, not dissatisfaction. A JAMA cohort study of 125,474 patients found 46.5% with type 2 diabetes and 64.8% without diabetes discontinued within one year, with higher income (>$80,000) significantly associated with lower discontinuation rates (HR 0.72). This creates a vicious cycle: patients who can afford continuous treatment maintain weight loss and its cardiovascular benefits; those who lose coverage regain weight and its associated health costs.

The political economy of appetite suppression

The policy landscape shifted dramatically in 2025–2026. The Trump administration initially rejected Biden's proposed Medicare coverage expansion in April 2025, then reversed course in November with a negotiated deal that married price concessions to tariff relief for Novo Nordisk and Eli Lilly. Robert F. Kennedy Jr.'s arc was equally whiplash-inducing: he testified in January 2025 that GLP-1 coverage could "cost over a trillion dollars a year" and advocated for nutrition-based solutions instead, then appeared at the White House in November calling the price deal "a momentous accomplishment."

The BALANCE Model, launching through CMS in stages from May 2026 through January 2027, represents the first systematic Medicare/Medicaid GLP-1 access framework. North Dakota became the first state to mandate insurance coverage in essential health benefits. But as of January 2026, only 13 state Medicaid programs cover GLP-1s for obesity.

IV. The Everything Drug Disrupts Every Industry

From grocery aisles to airplane fuel tanks

The downstream economic disruption is staggering in its breadth. Cornell's study found GLP-1 households reduce grocery spending by 5.3% and fast-food spending by ~8%. KPMG estimated caloric intake drops 21% and monthly grocery spend falls 31%. J.P. Morgan projects $30–55 billion in annual revenue reduction for the food and beverage industry by 2030–2034.

Companies are scrambling. Nestlé launched Vital Pursuit — its first new brand in 30 years — specifically for GLP-1 users: 14 frozen meals, high protein, portion-aligned, priced at $4.99 and under. Conagra added "GLP-1 Friendly" labels to 26 Healthy Choice products. The alcohol industry faces particular risk: the top 10% of drinkers account for nearly 60% of U.S. alcohol sales, and GLP-1s demonstrably reduce alcohol cravings. Morgan Stanley forecasts a 2% alcohol volume decline by 2035.

Bariatric surgery volumes fell 46.4% from Q3 2022 to Q3 2025, per a March 2026 JAMA Surgery study of 3.1 million patients. GLP-1 prescription rates among surgery-eligible patients jumped from 0.22% to 24.17% in the same period. Jefferies Research estimated that a 10% reduction in average passenger weight could cut total aircraft weight by ~2%, lower fuel costs by up to 1.5%, and save the top four U.S. airlines up to $580 million per year.

The "everything drug" keeps expanding its indications

GLP-1s are no longer just weight-loss drugs. The SELECT trial demonstrated a 20% reduction in major adverse cardiovascular events and 19% reduction in all-cause mortality in overweight/obese patients without diabetes — with benefits independent of weight loss magnitude. Zepbound became the first-ever FDA-approved medication for obstructive sleep apnea in December 2024, reducing CPAP initiation by 83%. Ozempic received FDA approval for chronic kidney disease in January 2025 (FLOW trial: 24% reduction in major kidney events). Wegovy was approved for MASH liver disease in August 2025 (62.9% resolution of steatohepatitis versus 34.3% placebo).

The neurological data is perhaps most provocative. A JAMA Neurology meta-analysis in April 2025 found GLP-1s linked to a 45% reduction in Alzheimer's risk across 26 trials involving 160,000+ patients. Nature Medicine's study of 2 million+ patients found reduced risk of addiction to alcohol, cannabis, opioids, and stimulants. Scientists at Nature Biotechnology proposed in 2025 that GLP-1s may be "the first longevity drugs", noting that roughly half their benefits appear independent of obesity reduction.

Denmark became a pharma-state

Novo Nordisk's dominance has transformed Denmark's entire economy. The company's share of Danish GDP surged from 1% in the early 1990s to 8.3% in 2024, reaching approximately 10% when indirect effects are included. Danish GDP expanded 3.7% in 2024 driven by pharmaceutical exports; it would have been approximately 0% without Novo Nordisk. Pharmaceuticals now account for 24% of total Danish goods exports and roughly 40% of the country's total exports.

But Novo's stock has experienced a roughly two-thirds decline from its peak, hitting a 52-week low of $35.85 on March 3, 2026. CEO Lars Fruergaard Jørgensen was ousted in July 2025. Meanwhile, Eli Lilly became the first healthcare company ever to reach a $1 trillion market cap in November 2025, driven by Mounjaro's explosive growth (Q3 2025 alone: $6.52 billion, up 109%) and Zepbound ($3.59 billion, up 185%). Economists compare Denmark's Novo dependency to Finland's Nokia era — a cautionary tale about national prosperity tethered to a single product category.

V. The Philosophical Undertow: Are We Solving the Right Problem?

The structural argument won't go away

The most uncomfortable critique of GLP-1 culture is that it constitutes the most expensive band-aid in pharmaceutical history. Ultra-processed foods account for approximately 60% of calorie intake in the U.S. and UK. Kevin Hall's NIH randomized trial demonstrated that an ultra-processed food diet led to approximately 500 extra calories per day consumed versus a minimally processed diet. U.S. agricultural policy has historically subsidized the cheap inputs that make processed food profitable. Food deserts persist in low-income communities. The food industry designs products to override satiety signals.

The New Atlantis captured the paradox in 2025: if the fundamental problem is "too many calories packaged into forms that are too delicious and ubiquitous," then GLP-1s are "an anti-hedonic response... they dampen the appeal of food, making the irresistible resistible." But the same publication conceded: "There is nothing else, no plausible lifestyle intervention or regulatory reform, available to help the tens of millions of people with obesity manage the consequences of living in a broken food environment."

UCL researchers argued that "multi-faceted policies, regulations, taxes and limits on UPF need to occur in tandem with development of accessible, subsidised and sustainable alternatives." The American College of Lifestyle Medicine, American Society for Nutrition, and Obesity Medicine Association published a joint advisory in 2025 calling for combining GLP-1s with structured lifestyle programs — a "both/and" position that acknowledges the drugs' efficacy while insisting on structural reform.

Conclusion: the molecule as Rorschach test

GLP-1 drugs are the rare phenomenon that is simultaneously a medical breakthrough, an economic restructuring event, a cultural flashpoint, and a class signifier. The global market will likely exceed $150 billion by 2030. Next-generation drugs like retatrutide promise nearly 30% weight loss. Oral formulations are demolishing the injection barrier. AI is generating thousands of novel peptide candidates in hours rather than months.

And yet: 40% of prescriptions go unfilled. Two-thirds of lost weight returns when patients stop. Fewer than 3% of eligible people receive treatment. The production cost is under $5; the list price exceeds $1,300.

What makes GLP-1s uniquely revealing is that they force every American institution to show its hand. The healthcare system reveals its pricing dysfunction. The insurance industry reveals its actuarial logic versus its stated mission. The food industry reveals its dependency on overconsumption. The body positivity movement reveals the limits of its convictions. Social media reveals its capacity to turn any medical intervention into identity content. And the class system reveals, as it always does, that the most transformative technologies reach the privileged first and the vulnerable last — if ever.

The open question for the next decade is not whether GLP-1s work. They work. The question is whether a society that produces both the cheapest calories in human history and the most expensive appetite suppressants can be described as functioning at all.

Share Your Voice

Join the conversation to share your thoughts and help others understand this topic better.

Join the ConversationCommunity Feedback

No comments yet. Be the first to share your thoughts!