How GLP-1 Drugs Are Reshaping America's Food System

From grocery baskets to grain futures, the most comprehensive analysis of how weight-loss medications are rewriting the rules of American food production, processing, and consumption.

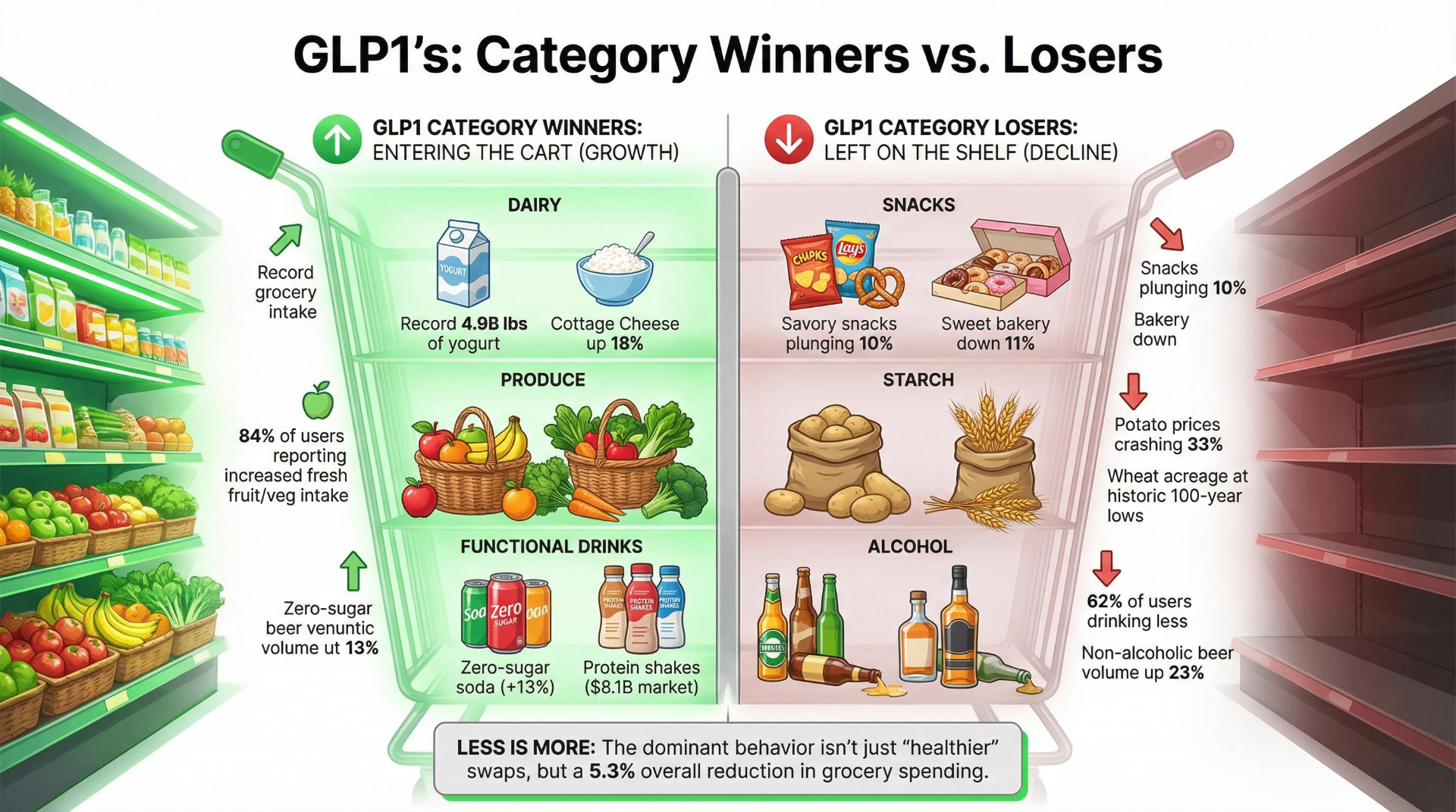

Roughly one in eight American adults now takes a GLP-1 receptor agonist, and their collective shift away from calorie-dense processed foods toward protein, produce, and smaller portions is sending measurable tremors through every layer of the US food supply chain. The disruption is no longer speculative: Circana reports that 23% of US households have at least one GLP-1 user as of late 2025, and projects those households will account for 35% of all food and beverage units sold by 2030. Cornell University's landmark study of 150,000 households found that GLP-1 adopters cut grocery spending by 5.3% on average within six months — with savory snacks plunging 10%, sweet bakery items falling 11%, and fast-food spending dropping 8%. Wall Street estimates the food-and-beverage industry faces a $30–55 billion annual revenue reduction by 2030–2034 (J.P. Morgan), while Morgan Stanley projects consumption of salty snacks, baked goods, and sodas could decline 3–5% by 2035. Yet the data also reveals important nuance: discontinuation rates remain high, aggregate US snack unit sales held steady through 2024, and many of the sharpest commodity-market declines have causes independent of GLP-1 adoption. This is a fast-moving story where early signals coexist with genuine uncertainty.

The adoption curve is steeper than anyone predicted

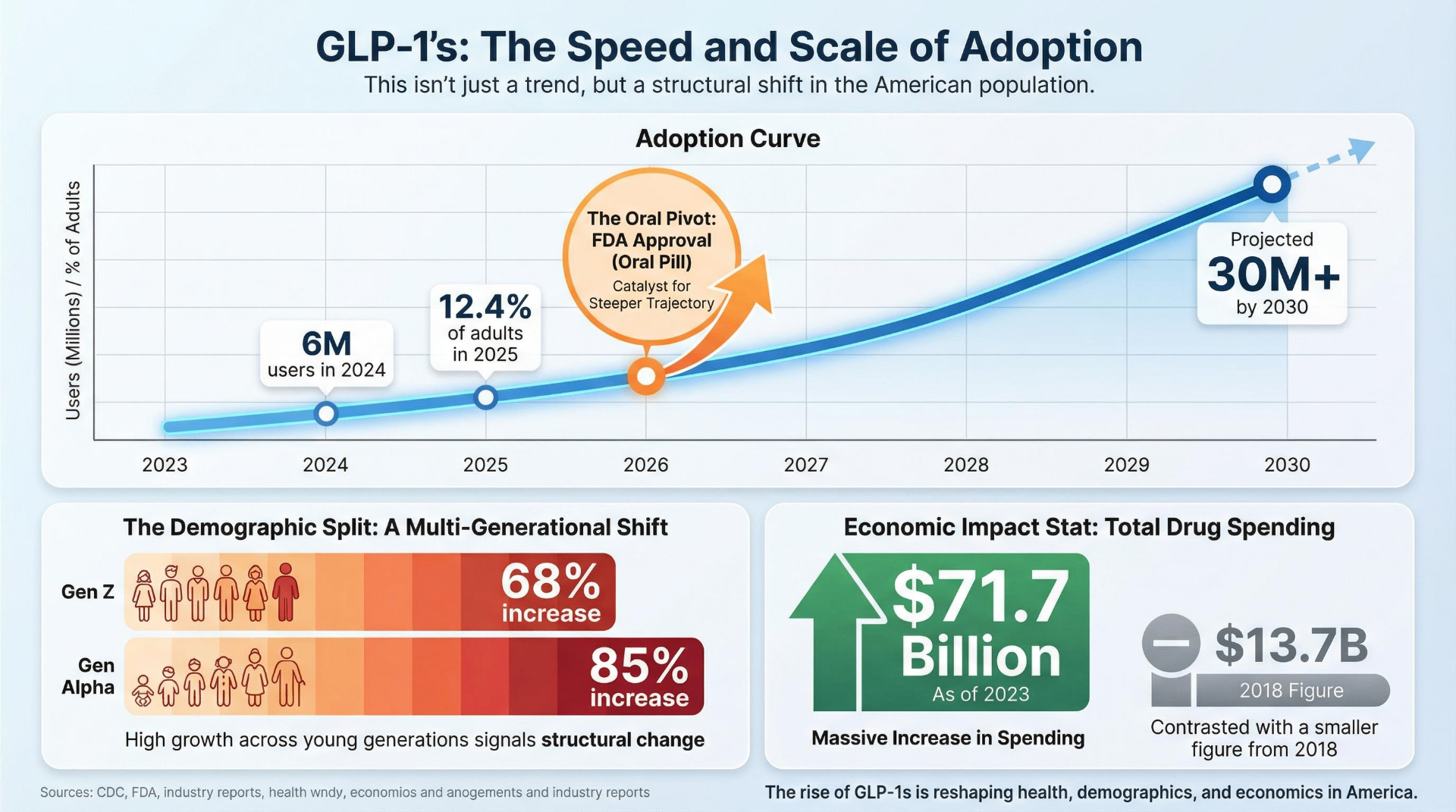

GLP-1 prescriptions have scaled with remarkable speed. Gallup's National Health and Well-Being Index recorded usage among US adults rising from 5.8% in February 2024 to 12.4% by mid-2025 — a doubling in roughly 18 months. J.P. Morgan estimates the active user base grew from approximately 5 million in 2023 to 6 million in 2024 and 10 million in 2025. Evernorth Research Institute data shows generational momentum: GLP-1 utilization grew 84.6% year-over-year among Gen Alpha and 67.8% among Gen Z, with weight-loss-specific prescriptions for those cohorts rising 142% and 178% respectively. Total US GLP-1 drug spending ballooned from $13.7 billion in 2018 to $71.7 billion in 2023, according to JAMA Network Open.

Projections diverge on the ceiling but agree on the direction. J.P. Morgan forecasts 25–30 million US users by 2030. Morgan Stanley projects 31.5 million by 2035 (~9% of the population). Goldman Sachs' baseline targets 30 million, with an aggressive scenario reaching 70 million. The December 2025 FDA approval of an oral Wegovy pill — now available at 70,000 US pharmacies — is expected to meaningfully accelerate adoption by removing the injection barrier and reducing cost. Medicare's BALANCE Model, launching in 2027, will further expand access by negotiating Ozempic, Rybelsus, and Wegovy prices down to $274/month (a 71% discount), with interim GLP-1 Bridge coverage beginning July 2026 at a $50 monthly copay.

The behavioral footprint of these drugs is substantial. Morgan Stanley's AlphaWise survey of 300 GLP-1 patients found users consume 20–30% fewer calories daily, with consumption of confections, sugary drinks, and baked goods reduced by as much as two-thirds. Clinical trials are even more striking: oral semaglutide at 50mg produced a 39.2% reduction in ad libitum energy intake versus placebo. The Cornell/Numerator study — the most rigorous purchase-data analysis to date — documented that the dominant pattern is buying less food overall, not wholesale substitution toward healthier options, though modest increases appeared in yogurt, fresh fruit, and nutrition bars. KPMG estimated GLP-1 users spend 31% less at the grocery store than before starting medication.

Processed food giants are scrambling to adapt

The packaged food industry is experiencing what may be its most significant demand disruption in decades. Nearly three dozen non-healthcare companies mentioned GLP-1 or weight loss on earnings calls in early 2026, up from 14 a year earlier and just 5 two years before that (LSEG data). The numbers tell a consistent story of volume erosion.

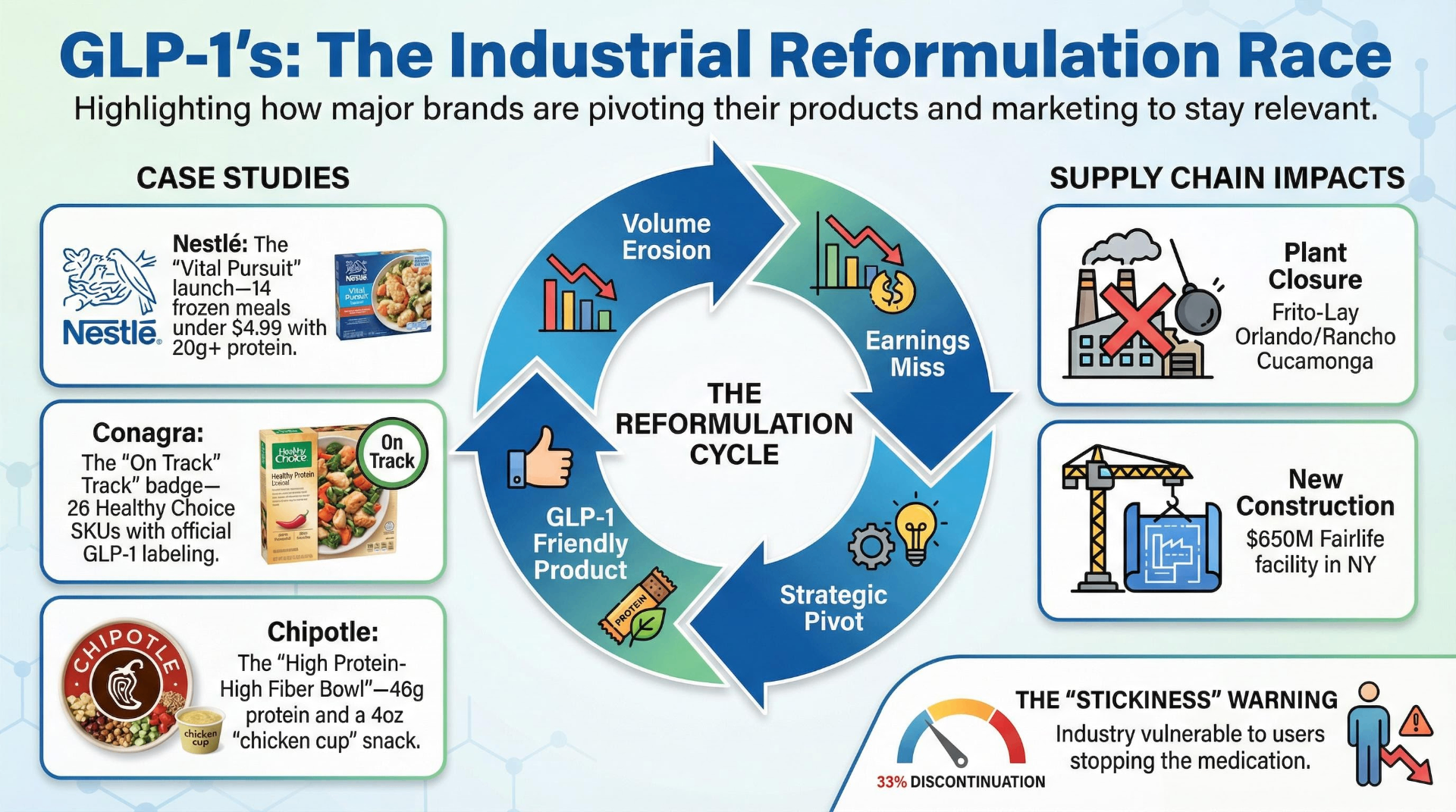

PepsiCo/Frito-Lay logged five consecutive quarters of volume losses through Q4 2024. Frito-Lay North America volume fell 3% in Q4 2024 and 4% in Q2 2024, with operating income declining 3.4%. TD Cowen documented that the salty snack category's compound annual growth rate collapsed from 7.8% (2019–2023) to effectively 0% in 2024. PepsiCo closed its Orlando Frito-Lay plant (454 workers) in November 2025 and announced the Rancho Cucamonga facility (248 workers) would shut by June 2026. CEO Ramon Laguarta acknowledged a "higher level of awareness in health and wellness is driving consumer shifts" while maintaining the company hasn't identified a "direct impact" from GLP-1s specifically.

General Mills suffered the sharpest market punishment. FY2025 North America Retail net sales fell 5% to $11.9 billion, with US Snacks down double digits. Its Q3 FY2026 earnings miss (March 2026) triggered an 18%+ stock decline in 30 days, eroding market cap from roughly $25 billion to $19.7 billion — a one-year total shareholder return of negative 33%. CEO Jeffrey Harmening stated plainly: "We expect GLP-1 and other anti-obesity drugs to have a lasting influence in the food and nutrition landscape, nudging some consumers towards smaller portions and more nutrient-dense protein and fiber-forward foods."

Mondelēz saw North America net revenue drop 4.1%, with CEO Dirk Van de Put citing a consumer shift toward grocery staples. Campbell's lowered its 2025 sales forecast after cookie and cracker sales failed to rebound. Conagra, however, has positioned itself as an early winner: its Healthy Choice meals labeled "GLP-1 friendly" are reportedly selling faster than rival products making similar claims.

The reformulation race is now fully underway. Nestlé's Vital Pursuit — its first new US brand in nearly 30 years — launched nationwide in Q4 2024 with 14 frozen meals featuring at least 20g protein at $4.99 or less. After updating packaging to prominently display "GLP-1 friendly," sales accelerated. Conagra placed an "On Track" badge on 26 Healthy Choice SKUs — the first major food brand to secure USDA approval for GLP-1-specific labeling. Danone launched Oikos Pro yogurt drinks with a patented Advanced Fusion Blend (23g protein, 5g prebiotic fiber, zero added sugar) explicitly targeting GLP-1 users. PepsiCo is developing a Propel product designed specifically for GLP-1 consumers with electrolytes, high fiber, and protein, alongside reformulations removing artificial ingredients from Lay's and Gatorade. EY-Parthenon estimates up to $12 billion in snack sales could be lost over the next decade.

Produce stands to gain, but the signal is complex

Fresh produce appears positioned as a structural beneficiary, though the evidence requires careful parsing. The Packer's Fresh Trends 2025 survey found that 84% of GLP-1 users reported increasing their produce consumption. NielsenIQ/Wells Fargo panel data showed fruit purchases up 14% and mixed vegetables up 38% among weight-loss GLP-1 users. UC Davis Innovation Institute data presented GLP-1 users consuming 55% more fruits and vegetables compared to pre-medication levels. Circana reported that produce was the only fresh department to increase its share of total store sales in 2024.

However, the Cornell purchase-data study injects important caution. It found only "modest increases" in healthier items like yogurt and fresh fruit among GLP-1 households, characterizing the dominant pattern as "less about switching to 'better' foods and more about simply buying less food." Self-reported survey data consistently shows larger dietary shifts than scanner-based purchase data — a divergence that suggests consumers may overstate their behavioral changes.

On the supply side, the picture is paradoxical. US fruit bearing acreage and utilized production declined approximately 13% over the decade ending 2024, settling at 15.9 million fresh equivalent tons. The American Farm Bureau Federation estimated billions in specialty crop losses in 2024 across almonds, apples, lettuce, potatoes, strawberries, and blueberries — driven by labor costs, climate events, and trade disruption, not insufficient demand. The exceptions tell a more positive story: blueberry acreage rose 9% versus 2015 (124,000 acres), with production up 33%; strawberry acreage climbed 5% to 61,000 acres.

Organic produce is the clearest growth pocket. US organic sales reached a record $71.6 billion in 2024, growing 5.2% — more than double the 2.5% overall market growth. Organic produce sales climbed to $21.5 billion, with organic berries hitting $2.1 billion (up 7.5%) and organic bananas crossing the $1 billion threshold. The Organic Trade Association explicitly cited "increased discretionary income from GLP-1 medications" as a growth driver.

Protein markets are the clearest beneficiary

The convergence of GLP-1 adoption, social media fitness culture, and clinical guidelines recommending 1.0–1.6g protein per kilogram for GLP-1 patients has created an unmistakable demand surge for protein-dense foods. A 2025 Bain & Company survey found 44% of US respondents want to increase protein intake, up from 34% in 2024. Cargill's 2025 Protein Profile reported 61% of Americans increased protein intake in 2024, up from 48% in 2019.

Dairy protein shows the strongest measurable signal. US yogurt production hit a record 4.9 billion pounds in 2024, up 6.3% from 2023, with another 6.7% gain through the first four months of 2025. Yogurt retail volume grew 9% in 2025, with dollar sales climbing 13.7% (Circana). Cottage cheese sales reached $1.75 billion for the 52 weeks ending February 2025, an 18% year-over-year increase, with protein-fortified variants growing 45% annually. AMPI is converting an entire cheddar cheese facility in Blair, Wisconsin to high-capacity cottage cheese production in 2026. Chobani generated over $3 billion in revenue in 2024, growing 20–25% year-over-year. Fairlife (Coca-Cola) reached $4 billion in 2024 revenue with a 22% US sales surge, prompting a $650 million new facility in Webster, New York to add 30% production capacity by 2026. The shelf-stable protein drink category hit $8.1 billion by November 2025, growing 14% annually.

Poultry benefits from both the protein trend and high beef prices. USDA projects broiler per capita consumption at 102.7 pounds in 2025 — the highest among all animal proteins. Tyson Foods' chicken segment sales rose from $20.5 billion to $21.6 billion in FY2025, with volumes up 3.8%. US cattle inventory, meanwhile, hit multi-decade lows at 86.7 million head in January 2025 (the lowest since approximately 1951), but this decline is driven primarily by drought, high input costs, and the natural cattle cycle — not GLP-1-induced demand destruction. Beef per capita consumption is projected to decline to 56.9 pounds in 2026, with supply constraints the dominant factor.

The protein supplement market — valued at $23.9–28.5 billion globally in 2024 — is projected to roughly double by 2032–2034. Ferrero Group's January 2025 acquisition of Power Crunch signaled that even traditional confectionery companies are pivoting toward protein snacks. Protein snacks are growing at three times the rate of the overall snacking industry.

Grains and starches face the most direct headwinds

This category presents the starkest intersection of GLP-1-driven behavioral shifts and concrete market data, though disentangling GLP-1 effects from other forces requires discipline.

Potatoes are the canary in the coal mine. US potato acreage for 2025 is forecast at 891,000 acres — the smallest since 1952, down 4% from 930,000 in 2024. Idaho, the dominant producing state, saw acreage fall 5% (315,000 to 300,000 acres), with some farms reporting 30% acreage reductions over three years. Idaho potato prices crashed from an average of $6.54 per hundredweight in 2024 to $4.40 in 2025 — a 33% decline. All three major frozen potato processors cut contract volumes 5–15% for the 2025 crop, with some growers "zeroed out completely." Hydrators reduced contracts by 30% or more. The Idaho Potato Commission CEO acknowledged: "2025 has been a struggle" due to "more supply than demand." Michigan Potatoes called the reductions "the most severe cuts most growers have ever experienced."

Lamb Weston, the dominant frozen potato processor, is in full restructuring mode. FY2025 Q2 net sales declined 8% to $1.601 billion, with adjusted income from operations dropping 42%. The company permanently closed its Connell, Washington facility, curtailed production lines, cut approximately 4% of its global workforce, and is targeting $55 million in annual savings. CEO Tom Werner cited "an accelerating rate of capacity additions and continued near-term softening of global frozen potato demand." Critically, Lamb Weston attributes demand softness primarily to menu price inflation reducing QSR traffic and the "fry attachment rate" declining, rather than explicitly naming GLP-1 drugs. Hamburger QSR traffic fell 6% in FY2024.

Wheat acreage is hitting historic lows. The USDA's March 2026 Prospective Plantings report showed 2026 all-wheat planted area at 43.8 million acres — the lowest since records began in 1919. Spring wheat acreage dropped to its lowest since 1970; durum fell 11%. Wheat futures traded near $553/bushel in July 2025, down from $723 in June 2024 and a $1,300 peak in May 2022. However, this weakness is primarily attributed to abundant global supply — record Argentine and Australian crops, competitive Black Sea pricing, and a strong dollar — not GLP-1-driven demand shifts. No analyst commentary directly linking wheat futures to GLP-1 adoption was found in this research.

Corn food use remains stubbornly stable at approximately 1,400 million bushels per year according to USDA data, and corn acreage decisions are driven by relative crop economics, ethanol demand, and exports. The CPI for rice, pasta, and corn meal decreased 1.1% in 2025, following a 1% decrease in 2024 — consistent with softening demand but not definitively attributable to GLP-1. The Corbion survey finding that 48% of GLP-1 users are buying bread less often and 37% reducing purchases of sweet goods provides the behavioral mechanism linking these drugs to grain-based categories.

Where the GLP-1 signal is clearest in this category is at the processed-product level: savory snack spending fell 10% among GLP-1 households (Cornell), sweet bakery spending declined 6.7–11%, and the salty snack category's growth rate flatlined after years of outperformance. The starch-heavy food categories are being squeezed from both directions — reduced demand and the reformulation imperative pushing manufacturers toward protein-forward alternatives.

Beverages are bifurcating between sugar and function

The beverage landscape reveals a dramatic split. Zero-sugar, protein-fortified, and functional drinks are surging while traditional sugar-sweetened beverages face persistent volume pressure.

PepsiCo's North American beverage volume declined for five straight quarters through Q4 2024. Coca-Cola's North America volume dipped 1% in Q2 2024 before recovering slightly. The growth engines are unmistakable: Coca-Cola Zero Sugar volume climbed 13% in Q4 2024, and Coca-Cola CEO James Quincey noted that "zeros and diets" — currently mid-teens percent of soft drink volume — could become a much larger share. Celsius rocketed 86% to $2.5 billion in FY2025 revenue, with its zero-sugar positioning resonating with health-conscious consumers. Zero-sugar energy drinks now account for roughly 50% of the energy drink category.

Alcohol shows the most clinically validated GLP-1 connection. A landmark Phase 2 randomized controlled trial published in JAMA Psychiatry (February 2025) found that semaglutide significantly reduced grams of alcohol consumed and peak breath alcohol concentration, with effect sizes potentially greater than existing FDA-approved alcohol use disorder treatments. A Nature Communications retrospective study of 83,825 obesity patients found semaglutide associated with 50–56% lower risk for both incidence and recurrence of alcohol use disorder. Morgan Stanley's survey found 62% of GLP-1 users drinking less alcohol. IWSR reported overall alcohol volumes declining nearly 3% in the first seven months of 2024. US non-alcoholic beer volume jumped 23% in 2024, up 175% since 2019, with Athletic Brewing commanding 52% market share at a valuation near $800 million. Constellation Brands' wine and spirits segment is in severe decline — net sales fell 14% in Q3 FY2025, shipment volumes dropped 16.4%, and the company took a $1.5–2.5 billion goodwill impairment. However, Molson Coors CEO Gavin Hattersley stated in April 2024 that the company doesn't "have data to suggest that [GLP-1] is having a meaningful impact on the alcohol space" — illustrating the difficulty of isolating GLP-1 effects from the broader Gen Z moderation and "sober curious" movements.

Protein beverages are the standout growth category. Fairlife (Coca-Cola) is on allocation to retailers because demand outstrips supply — prompting the $650 million Webster, New York facility. Core Power sales grew 39% by dollars and 29% by volume in the first nine months of 2024. The broader protein and meal replacement liquid category rose 11.1% to $4.7 billion (SPINS). PepsiCo is relaunching Muscle Milk and developing products including Doritos Protein, Quaker Protein, and a GLP-1-specific Propel formulation.

Retailers and restaurants are rewriting their playbooks

Major retailers have moved from observation to action. Walmart launched a dedicated "GLP-1 Support" online section featuring protein shakes, supplements, and digestive aids, while also operating a GLP-1 medication delivery program — giving it a dual revenue position as both pharmacy and food retailer. Walmart US CEO John Furner acknowledged seeing "a slight pullback in overall basket — just less units, slightly less calories" among GLP-1 users as early as October 2023. Kroger Health's Little Clinic began offering GLP-1 prescriptions starting at $99 per visit, with CFO Todd Foley confirming the company is expanding shelf space for high-protein and fiber products and adjusting planograms in response. Thrive Market added a GLP-1 filter for online shoppers in October 2025. Kantar data shows 46% of GLP-1 users have adopted a new primary grocery retailer, seeking stores that better align with their evolving dietary needs.

In food service, Chipotle made the boldest move, launching a "High Protein Menu" in December 2025 that explicitly cited "the rise of GLP-1s." The menu features a GLP-1-labeled High Protein-High Fiber Bowl (46g protein, 14g fiber, 540 calories) and a first-ever snack item — a 4-ounce High Protein Cup of chicken (32g protein, 180 calories). Smoothie King launched a seven-drink GLP-1 Support Menu in October 2024, each with 20+ grams of protein. Factor (HelloFresh Group) created an entire "GLP-1 Balance" meal preference category with chef-prepared, dietitian-approved, portion-controlled meals. Morgan Stanley rated healthier fast-casual chains — Cava, Chipotle, Sweetgreen, Starbucks — as best positioned, while indulgent QSR concepts like Jack in the Box, Wendy's, and Shake Shack face the greatest risk.

What Wall Street and the USDA actually see in the data

The analyst community has converged on a directional consensus while disagreeing on magnitude. Morgan Stanley projects consumption declines by 2035 of 5.3% for ice cream (the most affected category), 4–5% for chips, cookies, candy, frozen pizza, and regular sodas, and ~3% for alcohol, cereals, cheese, and frozen meals. J.P. Morgan projects a $30–55 billion annual food industry revenue reduction by 2030–2034. Roland Berger estimates a $55–90 billion impact on US grocery spending by 2030. The Gabelli Funds calculated that if 12–15 million patients reach GLP-1 medications by 2030, the cumulative effect would represent roughly a 1.8% headwind to total US caloric intake — meaningful but manageable for most categories.

The USDA, characteristically cautious, has been slow to formally incorporate GLP-1 into its demand models. At the February 2025 Agricultural Outlook Forum, USDA Chief Economist Justin Benavidez noted that snack unit sales held steady at approximately 10 billion units per year in 2024 — the same as 2020 — and stated: "I was surprised to see that when we think about the long-term trend towards GLP-1s' potential for less food consumption overall — we don't see that being born out in the data, just yet." However, the USDA acknowledged GLP-1 as a factor in sugar demand projections, noting domestic deliveries "face uncertainty from changing diets and from GLP-1 weight-loss drugs reducing consumption growth." No commodity group — National Corn Growers, American Farm Bureau, National Potato Council — has issued formal statements specifically about GLP-1-driven crop mix adjustments. The Purdue University Center for Food and Agricultural Business projected that lasting GLP-1 impacts could drive "regional diversification of crops, with less-processed foods grown closer to consumers," but cautioned that roughly 90% of the population remains non-users and consumer preferences remain taste-first, affordability second, nutrition third.

A critical nuance runs through all the data: approximately one-third of GLP-1 users discontinue medication within the study periods measured, and their spending reverts to pre-adoption levels. ADM research found 76% of users regained at least some weight after stopping. This attrition rate represents the single largest source of uncertainty in projecting long-term food system impacts. The oral pill formulation's lower cost and convenience may reduce discontinuation, but this remains speculative.

A structural shift with an uncertain amplitude

The evidence supports three confident conclusions and one honest uncertainty. First, GLP-1 drugs are producing real, measurable changes in food purchasing behavior — not merely self-reported intentions but documented transaction-level shifts in grocery baskets, restaurant spending, and category-level retail data. Second, the food industry has moved past denial into active adaptation, with Nestlé, Conagra, Danone, PepsiCo, Chipotle, and dozens of others investing billions in reformulation, new product lines, and GLP-1-specific positioning. Third, the impact is concentrated in specific categories — savory snacks, sweet baked goods, sugar-sweetened beverages, and alcohol face the steepest headwinds, while protein-dense dairy, poultry, functional beverages, and (to a lesser extent) fresh produce benefit.

The honest uncertainty is about amplitude. At current adoption rates (~12% of adults), the aggregate food system impact — roughly 0.7% of total US food spending — remains modest relative to other forces like inflation, private-label substitution, and global commodity supply dynamics. The potato market's distress, wheat's historic acreage lows, and Lamb Weston's restructuring are real, but primarily driven by factors other than GLP-1 adoption. The question is whether adoption climbs to 20–30 million users and oral pills collapse the remaining access barriers. If it does, the agricultural system faces a genuine demand recomposition — less starch, less sugar, more protein, roughly similar produce — that could reshape planting decisions, processing capacity, and supply chains at a scale not seen since the low-fat movement of the 1990s, but in the opposite direction. The food companies already reformulating are making a bet that this future is more likely than not. The early data suggests they are right.

Share Your Voice

Join the conversation to share your thoughts and help others understand this topic better.

Join the ConversationCommunity Feedback

No comments yet. Be the first to share your thoughts!